Being your own boss sounds awesome, right? But then… health insurance. It gets tricky. At Insurance 2ALL (yeah, we get it), we know the drill — finding decent health coverage when you’re self-employed is like solving a Rubik’s Cube blindfolded.

So here’s the scoop: we’re diving into all the options on the table, from those marketplace plans to your professional association group plans (yep, they’ve got those too). But wait, there’s more — we’re chatting about the key stuff to mull over when picking a plan, plus some insider tips to navigate the health insurance maze (and come out the other side) as a self-employed warrior.

Health Insurance Options for Self-Employed Individuals

So, you’re self-employed. Translation: no company health plan safety net. When it comes to health insurance, you’ve got a puzzle to solve. Let’s dive into options that won’t make you pull your hair out.

Marketplace Plans: Your Primary Option

First up – the Health Insurance Marketplace. Courtesy of the Affordable Care Act, this should really be your go-to. Those Marketplace premiums fly around depending on metal tiers – think bronze, silver, gold – plus the second-cheapest silver deal.

These plans? They’re pretty solid, covering everything from your essential health benefits to preventive care, pills, and mental health. And the kicker? Pre-existing conditions won’t lock you out.

Short-Term Plans: A Temporary Fix

Enter short-term health insurance plans. Patchwork solutions – starting from September 2024, expect a three-month starter pack, maximum four months if you count re-ups. Dirt-cheap compared to Marketplace plans, but not too hot on the coverage front.

HSAs and HDHPs: A Tax-Efficient Approach

Then there’s the High Deductible Health Plans (HDHPs) paired with Health Savings Accounts (HSAs). It’s the duo that gives you a tax break while paying for health needs. How much you or anyone can sock into that HSA? Depends on your HDHP coverage, age, and when you’re eligible.

HSAs work magic with pre-tax contributions, tax-free growth, and tax-free withdrawals for those medical bills.

Professional Association Plans: Group Benefits for Individuals

What about professional associations? They might have group health plans that offer good deals. Sometimes, they beat individual plans, but – plot twist – always compare them with Marketplace offerings. You want the sweetest deal, right?

There you go. We’ve dissected the health insurance smorgasbord for the self-employed. Next up, we untangle the factors you need to chew on when picking the plan that fits just right.

What Matters Most in Self-Employed Health Insurance?

Your Health Profile and Coverage Needs

So, you’re self-employed and thinking about health insurance. First up, what’s your health status? Got any chronic conditions lurking around? How often are you visiting the doctor? Planning any major procedures? (That’s gonna be a yes or no question, folks). Your answers here are gonna steer you towards the right coverage level.

Now, if the doc’s office isn’t your second home, maybe you go with a high-deductible plan. But… if you’re managing something chronic or popping pills regularly, then saddle up for a plan with lower out-of-pocket costs-could save you a chunk of change over time.

Premiums vs. Out-of-Pocket Costs

And let’s talk dollars and cents. You hear “monthly premiums” and think “that’s my guy!” but hold on-don’t skip the fine print. Deductibles, copayments, and coinsurance are the sidekicks you can’t ignore. That low monthly might have a hefty deductible sneaking up on you.

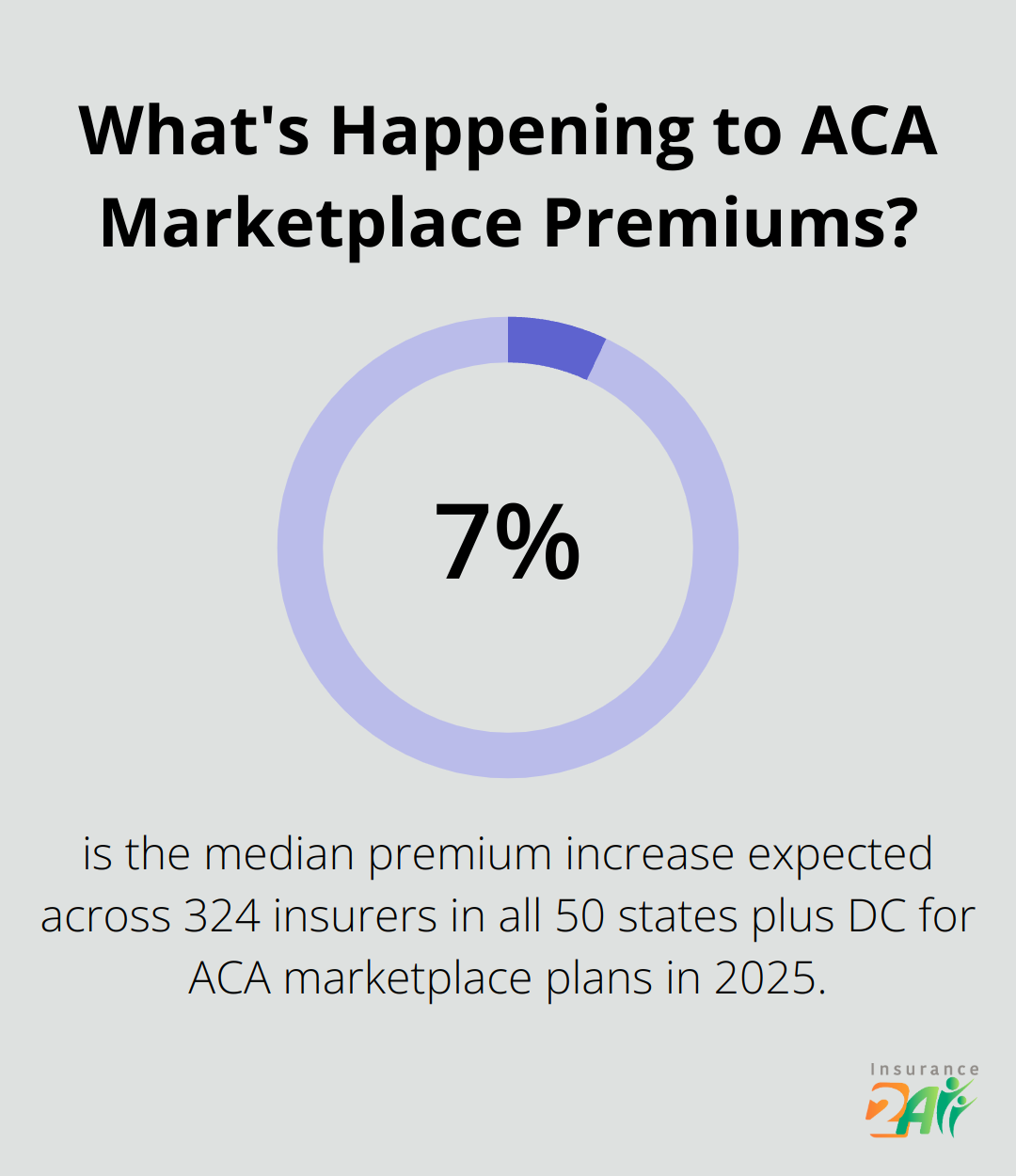

According to this analysis, we’re looking at a median premium spike of 7% in 2025-across 324 insurers, all 50 states plus DC. Yeah, it’s a jungle out there. Make sure you’re checking if you qualify for those sweet premium tax credits.

Provider Networks: Keep Your Doctors

Loyal to your doc? Better check that he’s in-network for the plans you’re eyeing. Out-of-network visits? They’re not cheap-they’ll slap you with substantial bills. Some plans (thinking PPOs here) give you more flexibility for your favorite docs-but it usually costs more.

Prescription Drug Coverage: The Devil’s in the Details

Let’s dive into your meds. Are you regularly restocking any prescriptions? Each plan’s got its formulary (fancy word for drug list). Gotta make sure your meds are covered and what tier they’re in. Spoiler alert: higher-tier drugs mean you might be shelling out even more cash.

Beyond the Basics: Dental and Vision

Dental and vision-often the unsung heroes. Most health plans leave these out, so if they’re your priority, be ready to snag separate policies. Some professional associations might cut you a deal on dental and vision with that membership card.

End game is finding a plan that covers what you need without draining your wallet-stay in budget? An insurance expert’s like your tour guide through this maze, helping match you with the right plan for the self-employed life. As you’re balancing these factors, let’s take a look at navigating the Health Insurance Marketplace-just for you, the self-employed warrior.

Mastering the Health Insurance Marketplace

Qualifying for Marketplace Plans

So you’re self-employed and wondering about the Health Insurance Marketplace? Here’s the deal: if you don’t qualify for Medicare, Medicaid, or any employer-sponsored plans, the Marketplace is your playground. You get to pick from various coverage levels-everything from the budget-friendly plans that kick in when things get real bad, to the spendier ones that offer a comfy coverage cushion.

Subsidies and Tax Credits: Financial Game-Changers

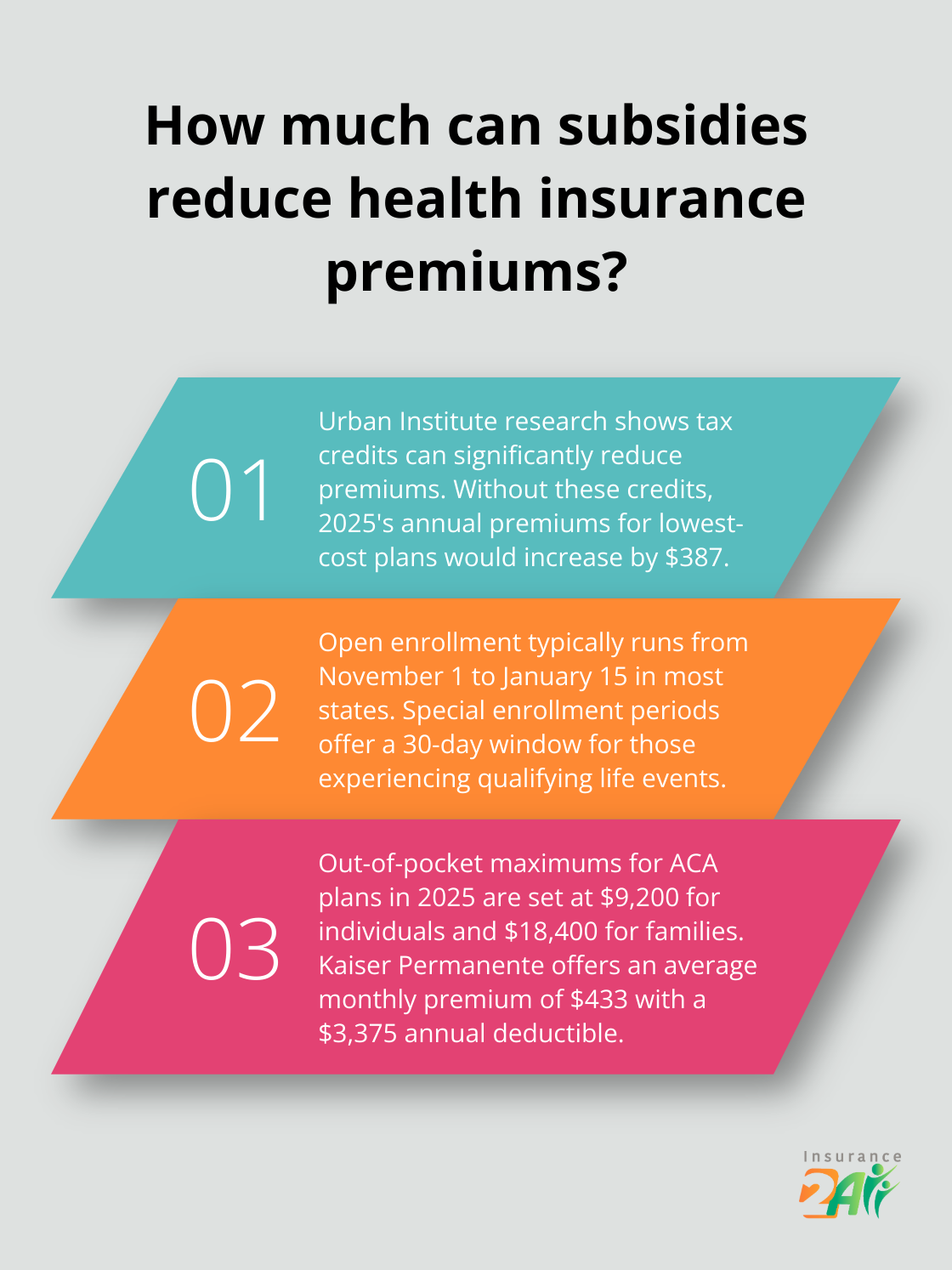

Let’s talk cash-subsidies and tax credits can seriously slash those premiums. Picture this: the Urban Institute says, without the extra tax credits, 2025’s annual premiums would balloon by $387 more for those lowest-cost plans.

Enrollment Periods: Timing Matters

Clock’s ticking-open enrollment typically runs from November 1 to January 15 in most states. Missed it? You’ll need a special enrollment period, triggered by life shake-ups like losing your job or hitting the big 2-6. That gives you a tight 30-day window to act.

Plan Comparison: Look Beyond Premiums

Evaluating plans? Don’t stop at premiums-dig deeper into total care costs. We’re talking deductibles, copays, out-of-pocket limits… the whole nine yards. For 2025, ACA plans peg these out-of-pocket ceilings at $9,200 if you’re flying solo and $18,400 for family coverage.

Use that “See plans and prices” tool on Healthcare.gov-it’s like a crystal ball for your docs and prescriptions to find plans that’ll support them. Avoid financial oopsies later and keep your healthcare dream team within reach.

Top-Rated Options for Self-Employed Individuals

What about top picks for the self-employed crowd? Kaiser Permanente shines bright with an average monthly premium of $433 and a $3,375 annual deductible. Molina Healthcare isn’t far behind, dangling attractive rates with a $426 average premium and a $3,640 deductible. (Pro tip: shop around multiple options to nail the perfect fit for you.)

Expert Guidance Available

Feeling lost in the Marketplace maze? You’re not alone. Get expert backup. Insurance 2ALL offers tailored guidance to find your ideal plan, with support every day of the week. Your health is priceless, and with a pro by your side, you’re poised to make the smartest decision for your unique situation.

Final Thoughts

So, here’s the deal with health coverage for the self-employed – a smorgasbord of options that can leave you more confused than a chameleon in a bag of Skittles. But don’t stress too much. It’s about finding what clicks for your health status, budget, favorite docs, and those meds you can’t live without. The Health Insurance Marketplace might just throw you a lifeline with subsidies and tax credits. A godsend if you ask me.

Timing, my friend, is everything. Open enrollment periods are the golden gates, and missing them means waiting for some life-altering event to jump back in. A chat with an expert? Could save you a coin or two, maybe a few headaches along the way. That’s where we step in – Insurance 2ALL. We’re here, rolling up our sleeves to help you snag the perfect coverage for whatever curveball self-employment throws your way.

Our squad is on standby seven days a week, ready to dish out the latest market scoop and a buffet of plans. We get it – being your own boss ain’t a walk in the park, especially when it comes to health insurance. Let us help you sidestep the landmines and cruise towards better health. Dive into your options and give us a shout. Your path to well-being could start here.