Job loss — it’s a punch to the gut. But losing your health coverage, too? That’s a second sucker punch you don’t need. With Insurance 2ALL, we’re here to cut through the noise and put you back in the driver’s seat on that health coverage highway.

We’ve whipped up this one-stop guide to help you untangle the jargon and zero in on what works for you. COBRA, Marketplace plans… we’ll sift through the mess to keep you covered while you get back on track. Let’s ensure you ride this bumpy transition with peace of mind.

What Are Your Health Insurance Options?

Losing your job-bummer, right?-but that doesn’t mean you’re kicked off the health insurance train. Let’s slice through the chaos and see what options you got to keep those health benefits rolling.

COBRA: Your Previous Employer’s Plan

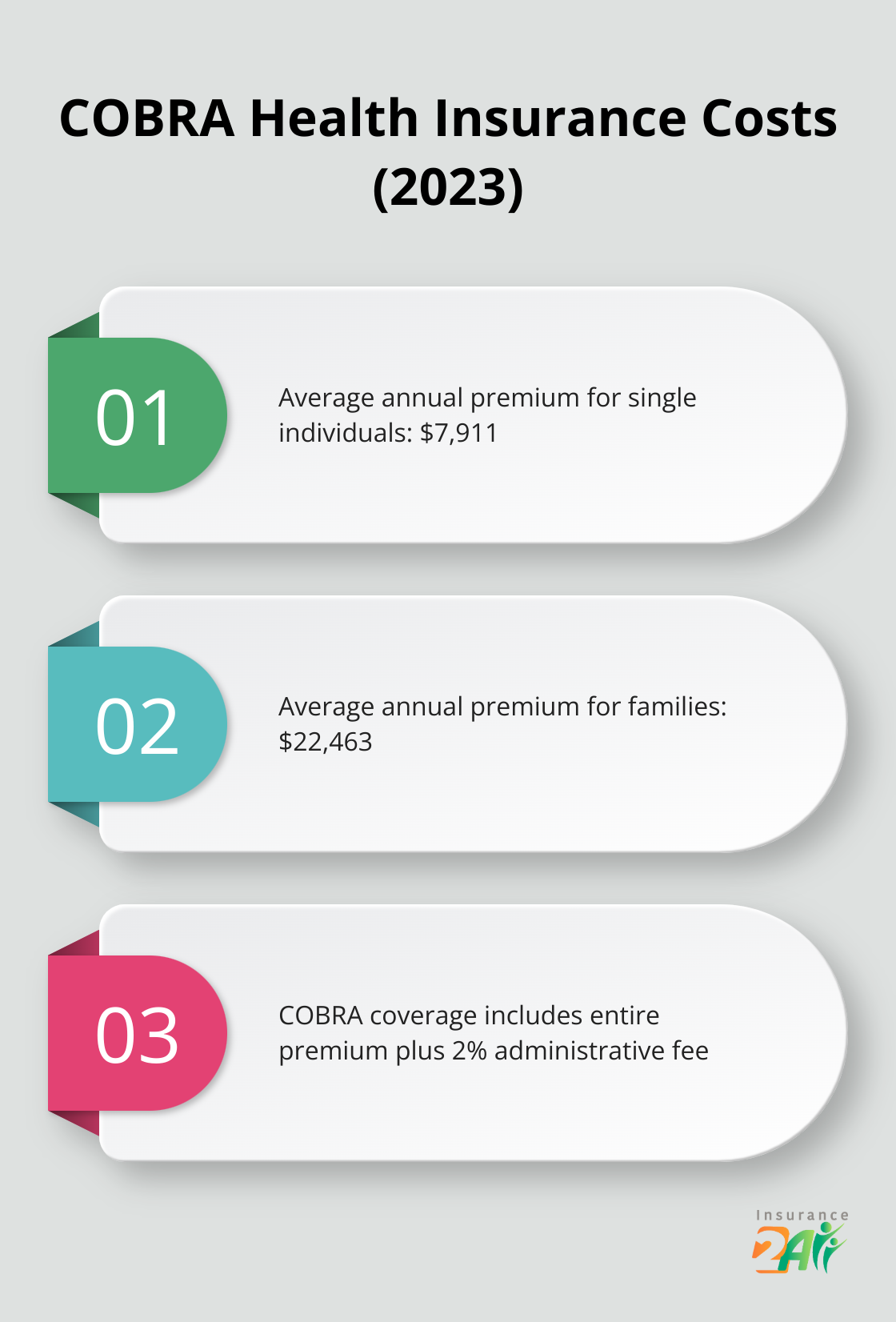

COBRA… sounds like a snake, but it’s your lifeline to your old health plan, letting you ride it out for up to 18 months. Quick and easy-but not cheap. You’re picking up the entire tab here, plus a 2% fee for good measure. Yep, that’s the whole shebang: the average annual premium in 2023 hit $7,911 for single folks and a hefty $22,463 for families, according to the Kaiser Family Foundation. With COBRA, you’re footing the whole bill.

Marketplace Plans: Affordable Care Act Options

Ah, the ACA (a.k.a. Obamacare)-the government’s way of tossing you a lifeline if COBRA’s got you wincing. Head over to Healthcare.gov and snag a plan with potential subsidies based on what’s in your wallet. Spoiler alert: it’s often lighter on your bank account than COBRA. In 2023, 7.8 million ACA Marketplace buddies needed a little extra help with Cost-Sharing Reductions (CSRs) and premium tax credits.

Medicaid: Low-Income Coverage

Income take a nosedive? Medicaid might swoop in to rescue you. Eligibility’s a patchwork thing depending on where you hang your hat, but usually, you’re in if you earn below 133% of the federal poverty line-think $19,391 for a solo gig or $39,750 for a family of four as of 2023.

Short-Term Plans: Temporary Coverage

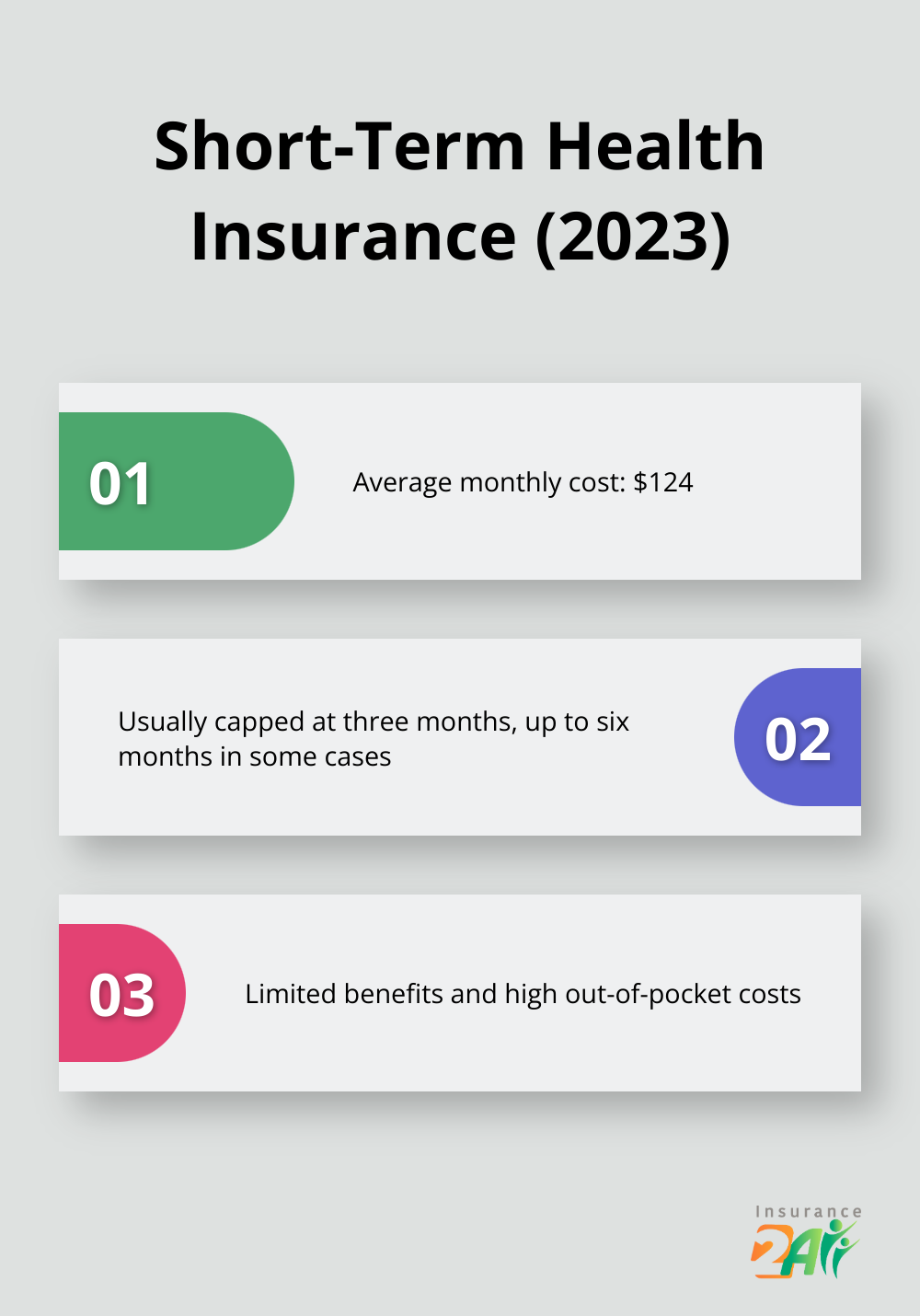

Short-term health insurance: think of it like a Band-Aid. They’re usually capped at three months, extending up to six if you’re lucky. Cheap upfront at about $124 a month in 2023 (eHealth says so), but you’ll trade the savings for sparse benefits. No love for pre-existing conditions here-and watch out for those sky-high out-of-pocket costs.

Comparing Your Options

Ready for a showdown? Line up your options and compare ’em like hungry kids at a candy store. Factor in premiums, what you’ll fork over for deductibles, and where the coverage taps out. And-pro tip-make sure your favorite docs and clinics play ball with your chosen plan.

Now that we’ve got the basics covered, let’s dive into navigating the Marketplace like a pro, especially if you’re flying solo without that cushy employer-sponsored safety net.

How to Apply for Marketplace Coverage

Seize the Moment: Special Enrollment Periods

Losing a job? Well, that flips open a 60-day window for getting yourself a Marketplace plan. Seriously, don’t procrastinate-get your application rolling pronto to snag this chance. Drag your feet, and you’ll be cooling your heels until the next open enrollment.

Calculate Your Income: Estimation is Key

Your wallet’s new bestie? An accurate income estimate. This little numero determines if you’ll score subsidies. Toss in unemployment benefits, any severance stash, and a crystal-ball look at future earnings. Nail it, or risk a nasty shock at tax time or, worse, kissing savings goodbye. Aim for precise, but if you’re floundering in doubt, be extra cautious.

Choose Wisely: Beyond Premium Costs

Think picking a plan is just about snagging the lowest premium? Think again. Dive deeper-consider your health shenanigans, go-to docs, and those sneaky out-of-pocket goblins. Low premiums sometimes hide hefty deductibles waiting in the wings. Bronze plans? Low premiums, but high costs on the flip side. Platinum flips the script.

Check out the Kaiser Family Foundation with its snazzy Health Insurance Marketplace Calculator and 2025 shiny premium data-it’ll help you size up insurance costs and subsidy potential. Scope it all out to squeeze every droplet of savings.

Navigate the Application: Step-by-Step Guide

- Head over to Healthcare.gov or your state marketplace turf

- Whip up an account and assemble your life’s paperwork (Social Security deets, cash flow stuff)

- Tackle the application-be thorough and truth-tossing

- Peep at your eligibility outcome-subsidies and plan choices, voilà!

- Go plan shopping-check ’em out side-by-side, look at premiums, deductibles, and the whole shebang

- Choose your champ plan, seal the deal

- Pay that first premium to kick-start coverage

Stuck in the mud? Don’t worry-free help’s within reach. Marketplace navigators and certified app whisperers can pull you through. Don’t be a stranger-it’s their gig to get you sorted.

Insurance 2ALL rides in with personalized help, every day of the week. Our squad can help untangle income riddles or size up plan picks, making sure you land the coverage that’s just right for you.

As you’re weighing your Marketplace game plan, keep an eye on alternative health insurance pathways that might just hit the sweet spot for your needs. Let’s peek into some quirky approaches to getting covered in the next section.

Unconventional Paths to Health Coverage

Health Sharing Ministries: A Faith-Based Approach

Let’s talk about health sharing ministries. They’re this quirky, non-profit twist on insurance-except they’re not actually insurance (important!). What happens here? Members throw in their monthly bucks into a communal pot. Then, when someone gets hit with a healthcare expense, everyone’s chipping in to help cover it. Simple, right? But heads up, legally, these aren’t health insurance… there are no guarantees on claims. And, yep, they’re sidestepping all those pesky regulations that come with traditional insurance plans.

But here’s the kicker-these ministries often come with some faith-based strings attached. There’s a chance they might say “nah” to pre-existing conditions or certain treatments. So, yeah, gotta squint at that fine print before you commit.

Part-Time Gigs with Health Perks

And guess what? You don’t have to be chained to a full-time gig for those sweet benefits. Some savvy companies are hooking part-timers up with health insurance. For instance, the American Red Cross-wear red, work 20 hours a week and you’re golden for health perks. Even big players like Costco and Lowe’s are in the game for part-timers.

So cruise through local job boards or the company websites… where part-time work meets health benefits and some extra cash. It’s a win while you’re hunting for that full-time unicorn job.

Student Health Plans: Not Just for Full-Time Students

Feeling the itch for more learning? Student health plans could be your secret weapon. Tons of colleges offer these wallet-friendly plans to students, and-get this-even part-timers can sneak in on the action.

Look beyond the big-name unis too. Community colleges or vocational schools could unlock these affordable health coverages for a class or two. That’s ROI, folks.

Piggybacking on Family Coverage

And here’s a sweet deal for the under-26 crowd-thanks to the Affordable Care Act, you can still hang onto your parents’ health plan. Great bailout for new grads facing those early career hiccups or job changes.

For the married crew, scan your spouse’s employer plan. It’s often a wallet-friendlier ride than going solo on individual plans. Plenty of companies let employees bring their spouses on board.

Remember, these alternatives have their perks, but they may not pack the punch of ACA-compliant plans. Weigh out the benefits, costs, and those pesky hidden limitations. Feeling swamped? Insurance 2ALL is like the GPS in this jungle, helping you find your best health coverage match.

Final Thoughts

Health insurance when you’re out of a job-what’s the game plan? Options, my friend. We’ve got COBRA, Marketplace plans, Medicaid, and short-term coverage on the menu. Throw in health-sharing ministries, part-time gigs with benefits, student plans, or mooch off the fam’s coverage. Your health and financial security are hanging by a thread here, so do us all a favor and hop to it-time’s ticking to keep those gaps in coverage at bay.

Start with the essentials: What do you need? What’s the budget? Dive into those options I just rattled off (watch those eligibility quirks, surprise costs, and fine print). The clock’s ticking louder than your uncle’s snoring when you’re trying to snag one of these plans post-job loss. So yeah, don’t put off locking down your insurance-your bank account will thank you for dodging those sky-high medical bills.

Need a lifeline for this health insurance maze? Hit up Insurance 2ALL. These folks are basically on speed-dial 24/7 to guide you through Obamacare and Medicare waters. With years-nay, eons-of experience, they’ll hook you up with affordable coverage that fits like a glove.