Health insurance costs—yeah, they can hit hard. At Insurance 2ALL, we often hear this: “Can I write off my health coverage on my taxes?” The answer? It’s not exactly cut-and-dried… depends on several things (your job status, your specific health plan… the works).

But don’t sweat it—we’re here to break it down. This post will cut through the legalese and get real about those health insurance tax deductions. You might just find a way to keep a bit more cash in your pocket come tax day.

What Counts as Tax-Deductible Health Insurance?

Out-of-Pocket Premiums

So, let’s dig into tax-deductible health insurance premiums. Generally, they include those you pay from your own pocket with after-tax dollars. If your employer’s ponying up with pre-tax dollars-nope, not deductible. But if you’re self-funding, guess what? You may get a break.

The IRS throws you a bone by allowing deductions for medical expenses (yep, health insurance premiums included) that tip over 7.5% of your adjusted gross income (AGI) for the 2024 tax year. And this isn’t just for you-it covers your spouse or dependents, too.

Eligible Health Insurance Plans

Here’s where things get interesting, folks. The IRS isn’t handing out deductions for every health plan on the planet. The usual suspects that qualify are:

- Individual health insurance policies

- Medicare premiums (Parts B and D-just play along)

- Long-term care insurance (but watch out for those age-based limits)

- Dental and vision insurance

Those Health Insurance Marketplace plans? They might sweeten the deal with extra benefits. Plus, if you’re flying solo without an employer-sponsored plan, you can often knock those premiums right off your taxable income. Sweet deal, right?

Self-Employed Individuals

Ah, the perks of being self-employed. If you’re running your own show, there are gold nuggets in the form of health insurance deductions. Go ahead and use Form 7206 to figure out what you can slide over to Schedule 1 (Form 1040), line 17.

But remember these two gotchas:

- Your deduction is capped by your business’s net profit.

- You miss out on this deduction for any month you had an employer-sponsored plan lurking around.

IRS Guidelines: The Details

The labyrinth of IRS rules, my friends. Here’s the lowdown on health insurance deductions:

- Want to claim medical expenses? You must itemize them on Schedule A of Form 1040.

- Only expenses you’ve paid out of pocket count. If you got reimbursed, it’s a no-go.

- Timing is the key. Deduct the premiums in the year you hand over the moolah, not when services are rendered.

And just when you think you have it down, tax laws shift gears. What works one year might not the next. The moral of the story? Stay on your toes-or team up with a tax pro to guide you through the IRA’s latest twists and turns.

Maximizing Your Deductions

How to juice those health insurance tax deductions? Check out these nuggets:

- Document every medical expense and insurance premium meticulously.

- Think about clustering medical procedures in one year to top that 7.5% AGI wall.

- And, give Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) a whirl for that extra tax advantage.

Getting the hang of these finer points can make navigating the convoluted world of health insurance tax deductions a breeze. Moving ahead, let’s drill down into calculating these deductions spot-on and making sure they fit nicely on your tax return.

Some folks switch it up with alternative health coverage-high-deductible health plans paired with direct primary care-to keep those healthcare expenses in check.

Crunching the Numbers on Health Insurance Deductions

Self-Employed? Here’s Your Silver Lining

So, you’re self-employed and swimming in the sea of premiums? Good news – that raft over there, the one called “deductions,” is your ticket. Self-employed folks can potentially deduct premiums paid for medical, dental, and some long-term care insurance (spouses and dependents, you’re covered too). This isn’t just any deduction-it’s the special kind that shows up on Form 1040, Schedule 1, Line 17… no itemizing shenanigans required. But-ah yes, the fine print-there are two speed bumps: the deduction stops where your self-employment income does, and forget about it if you had an employer-sponsored plan option during the same months.

Itemizing vs. Standard Deduction: The Showdown

Now, for the non-self-employed crowd-you’re not left out, but you do have to tussle a bit. To grab those premium deductions as medical expenses, you’ve got to itemize on Schedule A. Here’s the deal: only the amount above 7.5% of your adjusted gross income (AGI) matters. Say your AGI is $50K and medical expenses are at $5K… only $1,250 is in play ($5K – ($50K x 0.075)).

Fast forward to 2024-standard deduction sits at $13,850 for singles and $27,700 for joint filers. If your itemized numbers don’t leap past those figures, stick with standard… it’s the no-brainer choice.

Reporting Your Deductions: Don’t Miss a Dime

Turning the lens on reporting… precision is your best friend here. Those self-employed types? You jot down premium deductions on Schedule 1 of Form 1040. The rest of you? Schedule A’s your canvas for itemized deductions.

Remember-save those receipts and explanation of benefits (EOB) statements (because if the IRS had a love language, it would be documentation). If you’re with the Health Insurance Marketplace, you’ll get Form 1095-A, showcasing premium figures and any advance premium tax credits. It’s the key to spot-on deduction reporting or when you’re juggling premium tax credit reconciliations on Form 8962.

Navigating Tax Law Changes

Ah, tax laws… they’re like fashion-always changing. Keeping a tax pro in your corner ensures you’re snagging maximum deductions while staying within the lines of compliance.

Maximizing Your Health Insurance Tax Benefits

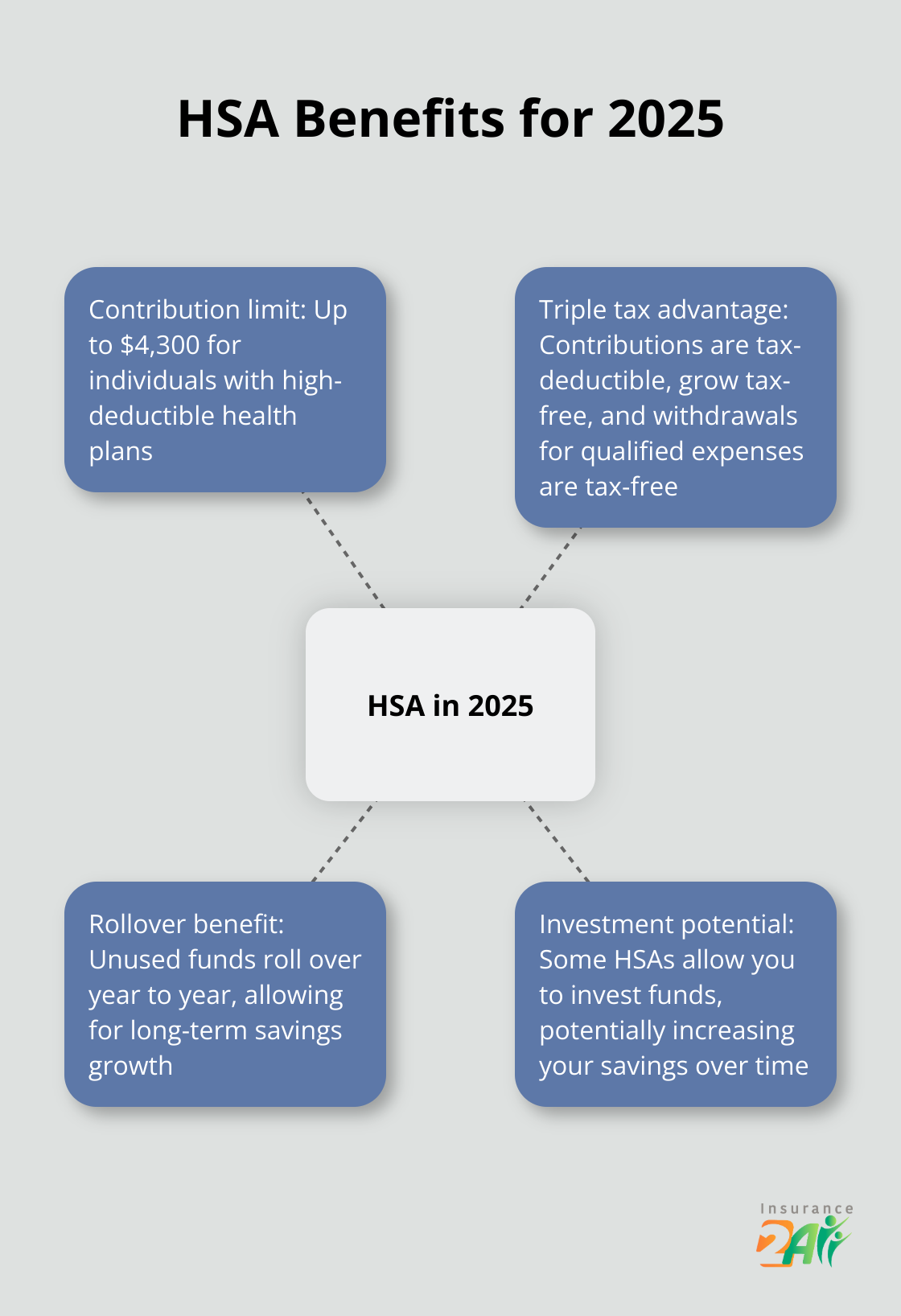

Want a pro-tip? Stack medical procedures in one calendar year to beat that 7.5% AGI threshold soundly. Use Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) to sneak in extra tax perks-these accounts let you stash away pre-tax dollars and pull them out tax-free for qualified medical escapades. By 2025, individuals with a high-deductible health plan can sock away up to $4,300 in an HSA.

Master these rules and keep tabs on your paperwork-you’ll watch that tax bill tumble. Onward, to how HSAs and FSAs can further unlock health insurance tax magic.

Curious about your premium landscape? Check out the Kaiser Family Foundation’s subsidy calculator, refreshed as of October 29, 2024. It’s like a crystal ball for the self-employed.

Supercharge Your Health Insurance Tax Benefits

HSAs: The Triple Tax Advantage

Let’s talk Health Savings Accounts (HSAs) – seriously, they’re like the winning trifecta of tax advantages. Check this out: not only do they help you stash those dollars for when retirement throws you a medical curveball, they also shave off a chunk from your tax liabilities. It’s a bit like winning the financial jackpot … minus the confetti.

Here’s the catch (there’s always a catch, right?): you need to have a high-deductible health plan (HDHP) to jump on the HSA bandwagon. For 2025, think $1,600 deductible for solo acts or $3,200 if you’ve got dependents in tow. Out-of-pocket cap? $8,050 for individuals and $16,100 for families. It’s not all doom and gloom-with HSAs, what you don’t use rolls over. Year after year, your medical rainy day fund builds ($$ grows!) and some accounts even let you invest those funds. Imagine turning your HSA into a little Wall Street.

FSAs: Use It or Lose It

Now, on to Flexible Spending Accounts (FSAs) – kind of like HSAs’ quirky cousin. They’re a different beast, but hey, perks exist. Your contributions take a nice little bite out of your taxable income. Here’s the scoop: unlike HSAs, FSAs demand you spend those Benjamins within the plan year (mostly). Some employers may hand out a grace period or a small rollover, but don’t bank on it. It’s all about strategic planning.

FSAs? They’re versatile – from copayments and deductibles to some neat medical gadgets. A neat twist? Some employers throw in dependent care FSAs, lightening the load for childcare or eldercare expenses. Gold star for them.

Optimizing Your Tax Benefits

Looking to squeeze every last drop of benefit from these accounts? Here’s the playbook:

- Crank those contributions up to the max. You’re not just saving tax dollars; you’re future-proofing against surprise medical bills.

- Record everything – and I mean everything. The IRS isn’t playing games when they want proof those withdrawals were legit.

- Got both an HSA and an FSA? Empty the FSA first. Keeps your HSA on growth mode.

- HSA holders – pay for minor stuff out-of-pocket and let your HSA grow. Reimburse years later (just ask for receipts, not hugs).

- Employer matches on HSAs? Grab them. Seriously, it’s free money plus tax perks.

Tax codes do their little annual shuffle – stay sharp, keep an eye out, and keep those strategies fine-tuned. Nail it with careful planning and you’ll not only slash healthcare costs, but your tax burden too. Better financial health? It’s in your reach.

Final Thoughts

Taxes – yeah, the stuff dreams aren’t made of. Health insurance tax deductions could shake up your bank account, big time. Is your health coverage tax-deductible? It’s like a difficult math problem… depends on your life situation and your plan, right? Enter the superhero: a qualified tax professional. They help squeeze out every deduction while also navigating those mysterious lands called HSAs and FSAs for more tax gold.

Insurance 2ALL understands health insurance isn’t just about the tax perks. Nope. It’s all about the right fit. They’re like your GPS in the wild jungle of health insurance – personalizing the journey just for you in this crazy complex world of policies. Need clarity on Obamacare, Medicare, and the like? They’re on the line every day.

Get savvy with tax strategies – pair ’em with the perfect health insurance, and watch your financial health blossom. Insurance 2ALL wants to ride shotgun on your road trip to discovering health insurance that clicks for you. It’s about trimming those premium and tax numbers while nailing down a plan that’s as solid as your favorite playlist.