Self-employed folks out there… yeah, that means you, gig gladiators and indie hustlers, face some wild challenges when it comes to health insurance. Let’s be honest, hunting down the best coverage can feel like trying to find a needle in a haystack. But here’s the deal—securing decent health coverage isn’t just a “nice-to-have,” it’s a must-have, an absolute fortress for your health—and your financial security.

Enter Insurance 2ALL. They get it. They absolutely comprehend the need for solid health insurance for those out on their own—entrepreneurs, freelancers, the whole independent shebang. So what’s the plan, you ask? This guide dives right into the crème de la crème of health insurance options for the self-made crowd and dishes out strategies to snag top-notch coverage… all while keeping those costs from spiraling into another universe.

Why Self-Employed Health Insurance Is Different

The Unique Challenges of Self-Employment

Alright, let’s dive into the wonderful world of self-employed health insurance – where you’re not just the boss of your business, but also the CEO of navigating your own healthcare. No cushy HR department to hold your hand. Nope, you’re on your own in this labyrinth, facing steeper premiums, skimpy coverage options, and a headache-inducing search for the “perfect” plan.

The Financial Balancing Act

Here’s the kicker – the cost. According to a 2024 study by the Kaiser Family Foundation, self-employed folks are shelling out an average of $8,951 annually for single coverage. Ouch. That’s a wallet hit, especially if you’re slogging through the early days of entrepreneurship or dealing with income that’s shakier than a politician’s promise.

Tailored Coverage for Specific Needs

Now, let’s talk bespoke. The one-size-fits-all plans usually don’t cut it. Picture this: a freelance graphic designer needing those eye exams like bread needs butter, or a lone wolf construction worker looking for solid accident coverage that won’t leave them in the dust. The trick? Finding a plan that checks all the health boxes without going broke. Easy, right? (Not.)

Deciphering the Multitude of Options

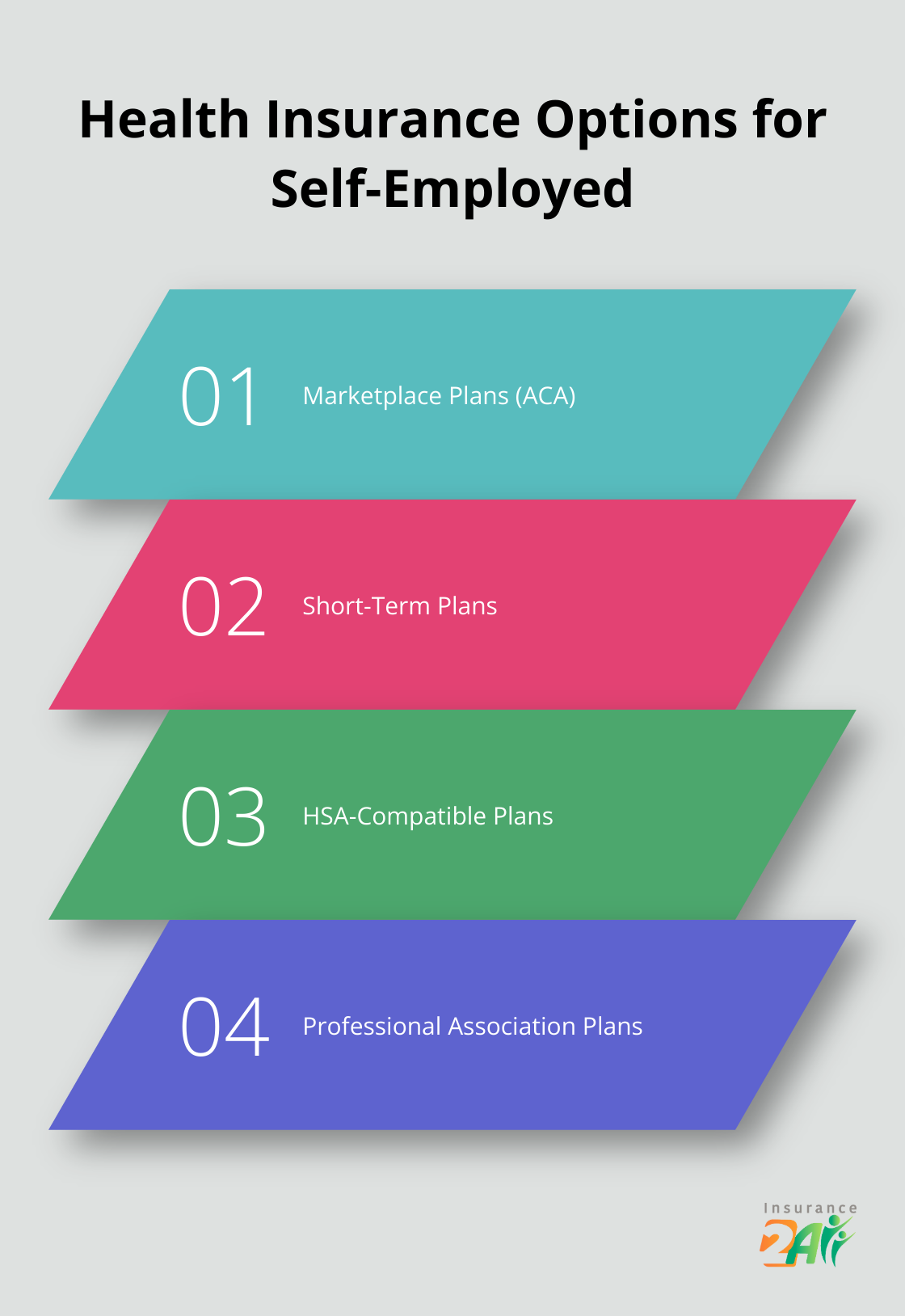

And just when you thought you had a handle on it, bam – you hit the options smorgasbord. Marketplace plans, short-term gigs, HSA-compatible this, group plans that – it’s like standing in front of an all-you-can-eat buffet where every dish tastes slightly of confusion. Each path has its ups and downs, so brushing up on these options is your ticket to not getting lost in the sauce.

Tax Considerations for the Self-Employed

Oh, and taxes. Yes, even here. The self-employed health insurance deduction can sweeten the pot by letting you deduct those premiums. Sounds great, but hold your horses – it means you’ve got to be on top of your records and the veritable maze that is the tax code. Fun times.

Preparing for Health Emergencies

And what about those health surprises (a.k.a. emergencies) lurking around the corner? Without a proper plan, it’s a fiscal cliff dive with no parachute. Coverage that covers both the everyday hiccups and the uninvited calamities is your lifeline.

So, as we wander through the myriad of health insurance avenues for the self-employed, let’s keep these unique hurdles front and center. Up next, we’ll unravel some of the popular choices for the self-motivated maverick, helping you stride through this convoluted jungle with a bit more swagger.

Popular Health Insurance Options for Self-Employed

You’re self-employed? Buckle up – selecting health insurance is like picking a needle out of a haystack, blindfolded. This chapter? We’re diving into the best routes to navigate this jungle of coverage options.

Marketplace Plans: The ACA Cornerstone

First stop: Affordable Care Act (ACA) marketplace plans. Think of them like the Big Mac of health insurance – a staple. Comprehensively covered? Check. Pre-existing conditions? Not a problem. And if the dollars aren’t flowing, there’s a decent chance you could snag some subsidies to ease the financial burn. The Kaiser Family Foundation’s subsidy calculator (freshly updated on October 29, 2024) can crunch the numbers on what those premiums might look like.

Now, if subsidies hit the snooze button, you’re shelling out – the sticker price for a silver plan for a 40-year-old in 2024? Around $456 a month according to HealthPocket. Not exactly pocket change for our strapped-for-cash self-employed amigos.

Short-Term Plans: A Quick Solution

Enter short-term health insurance plans – the quick-fix, duct-tape solution. They’re more for the “I need something ASAP” crowd who are between gigs or in health insurance limbo. Light on the wallet, but also light on the coverage, missing essentials like preventive care or your meds.

The catch? Yeah, there’s always one. These plans can give the cold shoulder to pre-existing conditions and slap on coverage caps. In 2024, short-term plans averaged about $124 a month. Cheap? Sure. But dare to imagine those out-of-pocket costs if you actually need real medical attention – they skyrocket.

HSA-Compatible Plans: A Tax-Efficient Approach

Next up, Health Savings Account (HSA) compatible plans – now we’re talking strategy. High-deductible health plans let you toss pre-tax dollars into an HSA to use for medical expenses. As of January 23, 2025, if you’re under these plans and a few other setups, you can keep stacking cash in there.

Why HSAs are cool – triple tax benefits, my friend. The dough you throw in? Tax-deductible. It grows and spends tax-free, too, as long as you’re focused on medical costs. But heads up, these plans usually mean high deductibles, which means you better be generally healthy or fine with paying out-of-pocket on the reg.

Professional Association Plans: Collective Bargaining Power

Now for professional associations – imagine them like a team huddle for better insurance deals. They pool members together to snag better rates and broaden coverage options. Take the Freelancers Union, offering health plans that could keep a few hundred bucks in your pocket each month compared to hunting solo.

So what’s the fine print? You gotta join the club, which might mean forking out for membership fees. And here’s the kicker: not every association has health insurance on their menu, and quality? All over the place.

Given all this – finding that magic insurance fit as a self-employed warrior? It’s a grind. That’s why Insurance 2ALL is here. We’re all about steering you through these murky waters, culling the noise to find what truly lines up with your needs and wallet. We’ve got our finger on the pulse of market shifts and policies, just so you can make that decision with confidence.

Up next, we’ll tackle cost-cutting strategies that’ll let you milk your coverage while keeping the pain in the wallet to a minimum.

How to Slash Your Health Insurance Costs

Self-employed folks usually see health insurance as a punch to the wallet… and for good reason. In 2024, grabbing individual health insurance set you back an average of $7,470 (eHealth report). But there’s hope-cut those costs without losing out on solid coverage.

Shop Around and Compare

Don’t just grab the first plan that lands in front of you. This insurance game is like a bazaar-lots of players, lots of prices. Fire up those comparison tools to lay plans side by side. Dig deeper than just the monthly premium-check out deductibles, copays, and those sneaky out-of-pocket maximums. A cheaper premium might turn into a money pit with sky-high deductibles.

Leverage Tax Advantages

Self-employed folks… you’ve got a secret ace: tax deductions. You can slice off 100% of your health insurance premiums from your tax return, saving you a hefty chunk. This covers medical, dental, and long-term care insurance for you, your spouse, and dependents.

Opt for a High Deductible Health Plan (HDHP) and pair it with a Health Savings Account (HSA). In 2025, shovel in up to $4,300 for individual coverage or $8,550 for family coverage into your HSA. These contributions? Tax-deductible. They grow tax-free and can be pulled out tax-free for legit medical expenses. Jackpot.

Consider Alternative Options

Enter health sharing ministries-gaining a fan base among the self-employed. These faith-based groups pool members’ monthly “shares” to cover medical bills. Technically not insurance, but they can be way cheaper. Some ministries start plans at a cool $199 a month for singles.

But hold your horses. These aren’t your regular insurance companies-less regulation and more rules about pre-existing conditions. Read every word of that fine print before jumping in.

Negotiate and Save

Don’t be shy about haggling. Many healthcare providers are open to discounts if you whip out cash or negotiate upfront.

Always ask for itemized bills-get those magnifying glasses out. Medical Billing Advocates of America reckon up to 80% of medical bills have errors. Spotting these mistakes? Could leave you with a wallet that’s not empty.

Explore Professional Associations

Got a professional association? They might offer group health insurance plans for members. These often beat individual plans-better rates, more comprehensive coverage. Do some detective work on associations in your field and weigh their offerings against other options.

And if you’re spinning your wheels trying to navigate this, Insurance 2ALL is your go-to. They specialize in helping self-employed folks find that sweet spot where comprehensive coverage meets affordability. Their team’s ready to guide you through and help you make a smart choice.

Final Thoughts

Alright, let’s tackle this head-on. If you’re one of those self-employed folks out there hunting for health insurance-you’re on a quest punctuated by unique hurdles. What you’re aiming for? That sweet spot where comprehensive protection meets affordability. We’re talking Marketplace plans, short-term options, HSA-compatible plans, and professional association group plans-all at your disposal. It’s like walking through a buffet of choices catering to different needs and budgets.

You wanna get savvy? Get cozy with a thorough plan comparison, think about tax advantages, and dig deep into alternative options-these tactics can really slash costs. And, heads up, the health insurance landscape isn’t static; it’s like a chameleon, always shifting. You gotta roll with it-review your coverage every year, reassess your needs. Why? New regulations, new plan options, and market trends are popping up like daisies-they could switch up the ideal solution for your situation.

Enter Insurance 2ALL-your go-to for personalized guidance. They’re out there, helping the self-employed navigate their way to comprehensive, affordable health insurance. Their squad of experts is on call seven days a week. They tackle your concerns and help nail down the perfect plan. So, with a solid strategy and the right resources, you can lock down health coverage that shields your well-being and fuels your entrepreneurial dreams. Boom.