Alright, folks, let’s talk small businesses and health insurance—a pairing as tricky as assembling Ikea furniture without the instructions. At Insurance 2ALL, we’ve got your back, because we know that snagging killer talent often boils down to one thing: benefits, baby.

This little manifesto of ours dives headfirst into the health insurance jungle out there for small businesses. We’re talking everything from your conventional group plans (yawn) to those funky, new-age options like Health Savings Accounts. And, hey, we’re not stopping there. We’ll chew over how to pick the sweet spot in coverage—balancing fiscal sanity with keeping your team smiling.

Small Business Health Insurance Options Demystified

Group Health Insurance Plans: A Traditional Approach

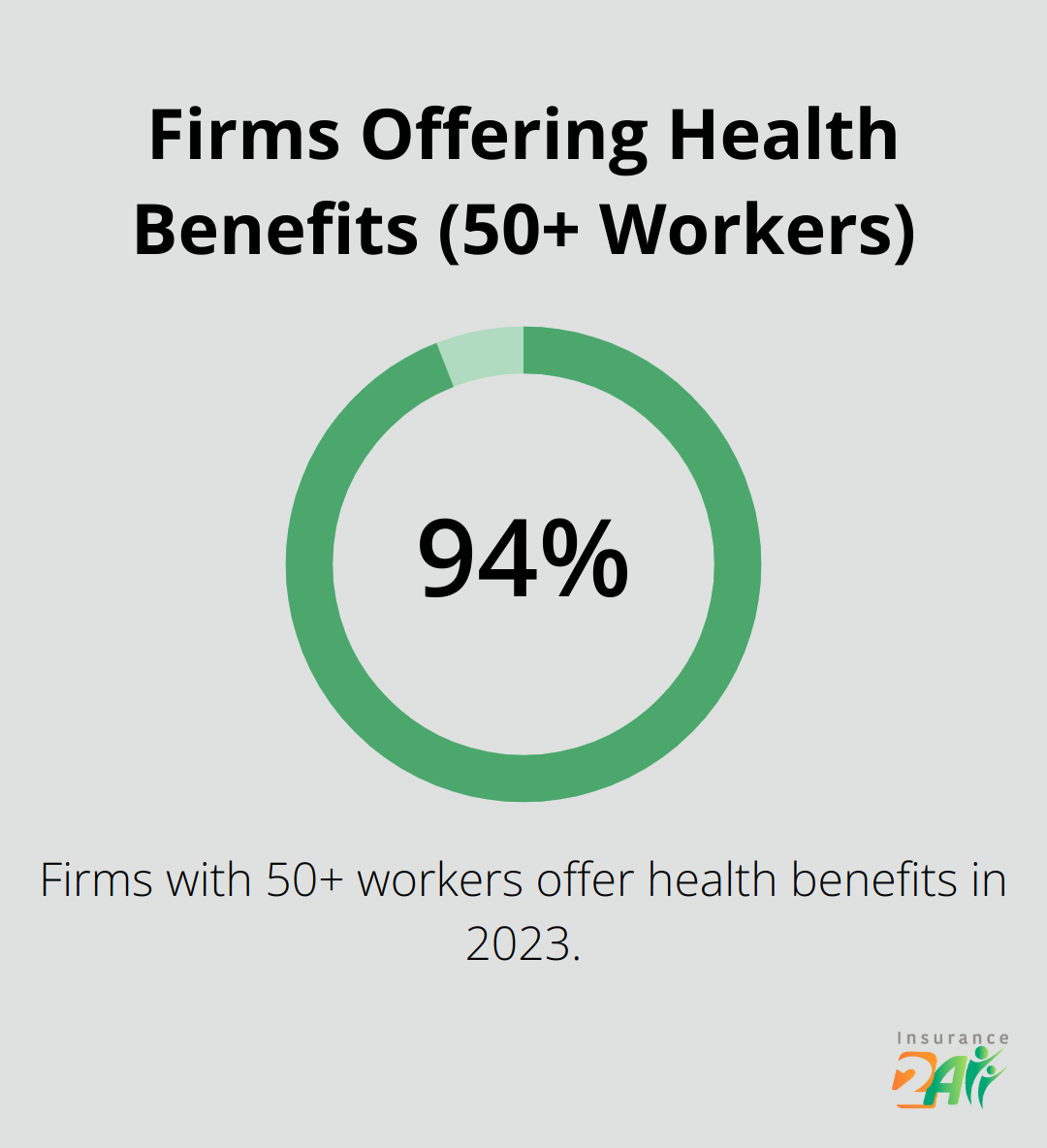

Let’s talk group health insurance plans-kind of the bedrock for small businesses when it comes to insurance, right? Over 94% of firms with 50 or more workers offer health benefits in 2023. Why? Because they spread risk across employees which can help shave off some costs. But, and it’s a big but, they might still be too pricey for the smaller guys.

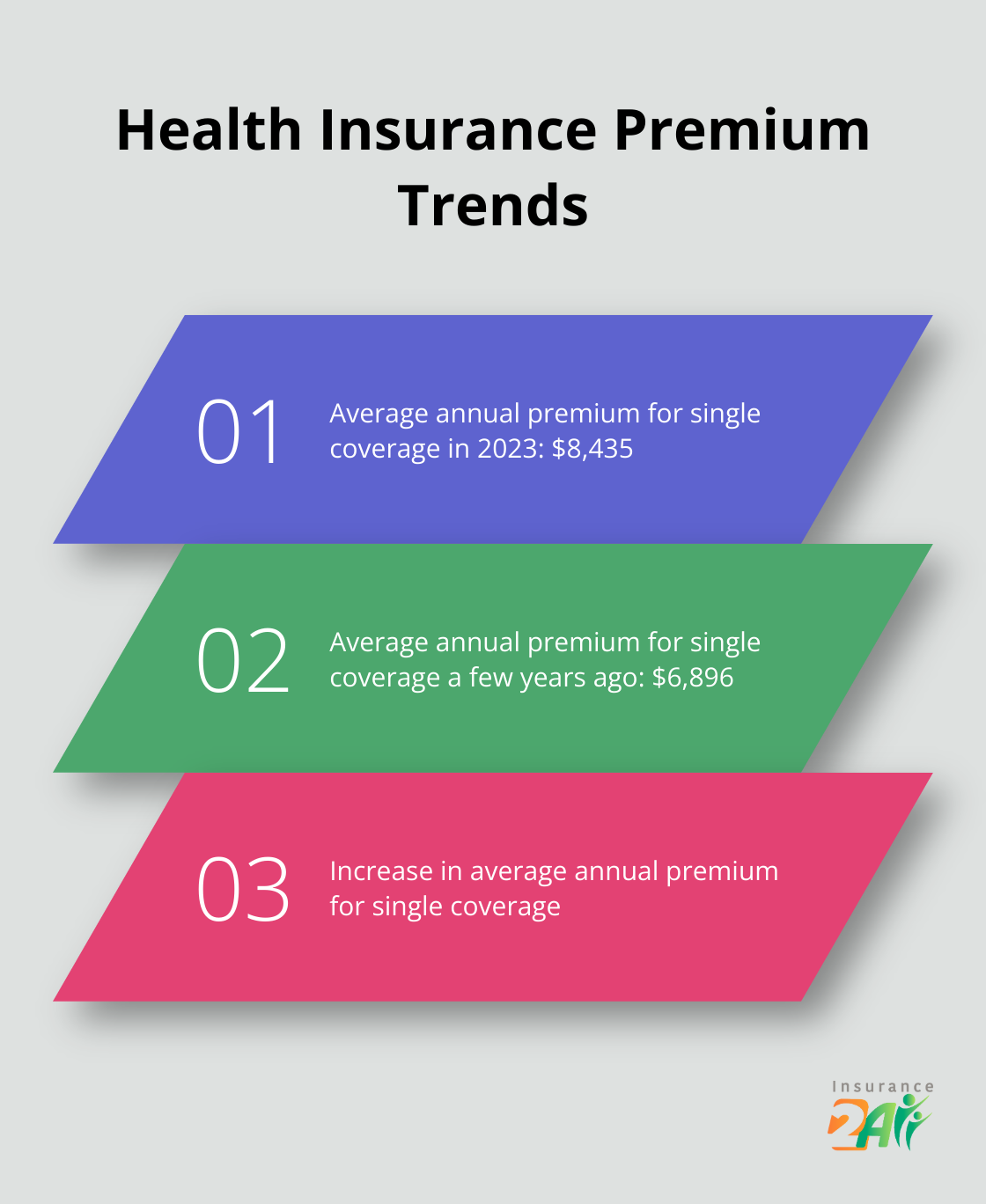

Check this out: the average annual premium for single coverage hit $8,435 in 2023, up from $6,896 just a few years ago (KFF). Ouch. So what’s a savvy small business to do? Some are turning to high-deductible plans with lower premiums-basically, dodging the price hikes a bit.

Health Savings Accounts (HSAs): A Tax-Advantaged Option

Enter HSAs, making high-deductible plans look a lot better. They let employees stash away pre-tax dollars for those pesky medical bills. In 2025, that’s $3,850 for individuals and $7,750 for families.

And here’s the kicker: Health Savings Accounts (HSAs) offer a triple tax advantage. Yep, you heard right. Tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses. It’s like finding a unicorn in the insurance world-a win-win for everyone. Employers even get a break on payroll taxes if they set up HSAs for pretax contributions.

Self-Funded Health Plans: Taking Control of Costs

Self-funding-no longer just for the big dogs. More small businesses are giving this a shot, paying claims directly instead of tossing money at an insurance company.

It can be a money-saver if your team is pretty healthy. But beware-a big health crisis could hit your wallet pretty hard. That’s why some small businesses go for level-funding plans, capping those potential losses. Smart move, right?

Professional Employer Organizations (PEOs): Strength in Numbers

PEOs are all the rage these days. They let you offload HR duties, including the whole health benefits mess. And by pooling small businesses together, guess what? PEOs can often snag better insurance rates. Score!

According to a study by the National Association of Professional Employer Organizations, businesses using PEOs grow 7-9% faster and have 10-14% lower employee turnover. Not bad odds, I’d say!

Choosing the right path depends on a bunch of stuff-your business size, who you’ve got working for you, and of course, your budget. Don’t sail these stormy insurance seas on your own. Call in the experts like a broker or Insurance 2ALL for the 411 that fits you to a T. Looking ahead, let’s dig into why giving health insurance to your team could be one of the best things for your biz.

Why Health Insurance Is Your Secret Weapon

Attracting Top Talent

So, small businesses want to play with the big dogs in hiring? Health insurance is your secret sauce. In 2025, a lot of companies are really digging into their leave policies to better support their employees, especially women and caregivers. Newsflash: This trend is hot, and you should totally be paying attention to it.

The Productivity Boost

Here’s the deal: employees with health insurance actually go to the doctor before things get ugly. That means fewer days off and more gettin’ stuff done. The CDC Foundation says companies bleed $225.8 billion annually because folks are out sick. Give them health insurance – you’re not just protecting them, you’re bolstering your profit margins.

Tax Benefits You Can’t Ignore

And hey, health insurance isn’t just good vibes – it’s money back in your pocket. Small businesses can deduct premium costs from federal taxes. Plus, if you’ve got fewer than 25 full-timers, check out the Small Business Health Care Tax Credit. Uncle Sam practically high-fives you for this one, covering up to 50% of those premiums.

Staying on the Right Side of the Law

About regulations: The Affordable Care Act lets you off the hook if you’ve got fewer than 50 full-time employees. But hold up, some states have their own rules. Take Hawaii – hire one person, you’re on the hook for health insurance. Compliance isn’t just dodging fines – it’s about being that responsible, stand-up employer your community needs.

A Strategic Move for Your Business

Health insurance – it’s not a “nice-to-have” anymore, it’s your ace in the hole in the biz world. Want talent? More productivity? Sweet tax wins? This is your play.

So, now that you’re all amped up on why health insurance is the jam, let’s get down to the details of picking the right plan for your crew. The next section? A roadmap to nailing it – meeting your business needs and making your employees happy.

How to Pick the Perfect Health Coverage for Your Team

Know Your Team Inside Out

First things first-understand your employees’ health needs. Why? Because one size does not fit all. Send out an anonymous survey. Find out about their health concerns, their favorite doctors, and the benefits they just can’t live without. This isn’t just about ticking boxes-it’s about making sure the coverage actually fits your team.

Maybe you’ve got a younger crowd-they might lean towards lower monthly premiums. Families? They’re likely willing to shell out more for broader coverage.

Crunch Those Numbers

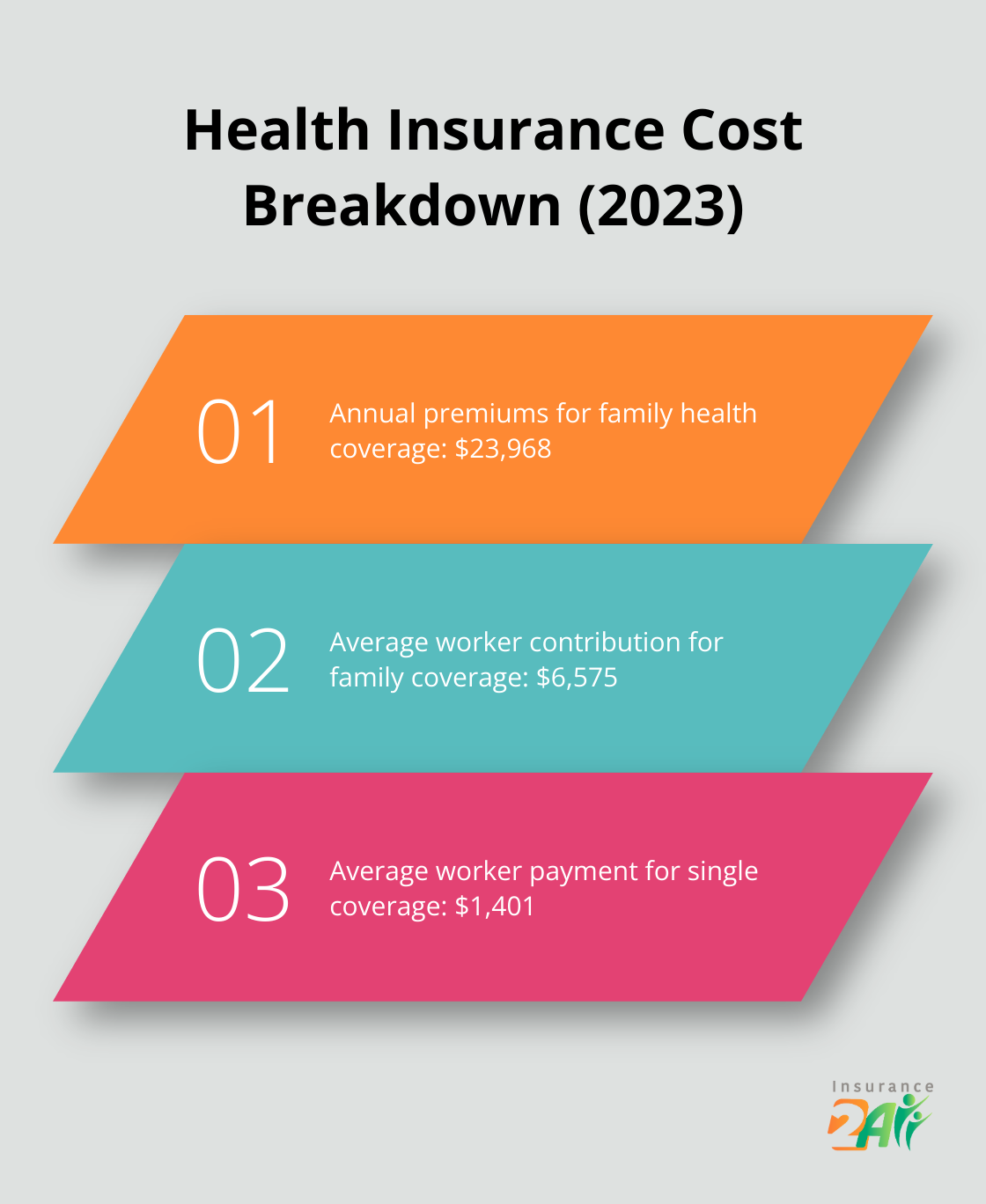

Money, it’s always about money, isn’t it? According to the Kaiser Family Foundation, annual premiums for family health coverage hit $23,968 in 2023. Workers? They’re coughing up $6,575 on average.

Small biz pro tip: you don’t need to foot the entire bill. Most places have employees chip in. In 2023, the average worker paid $1,401 for single coverage.

Play around with cost-sharing ideas. Maybe you cover 80% for single coverage and 60% for family plans. Or go with a flat amount regardless of the plan. The sweet spot? It’s finding what works for both your budget and your employees’ pockets.

Flexibility is King

Forget cookie-cutter plans-they’re dinosaurs. We’re in the era of flexible plans. Give options. A high-deductible deal with a Health Savings Account can be perfect for the young and healthy. A more all-encompassing plan? That’s for those who need ongoing care.

Some insurers have mix-and-match plans-employees tweak their own coverage. It’s more work up front, sure, but it cranks up employee satisfaction.

Bring in the Pros

Health insurance-it’s a maze. A broker or consultant? They’re your GPS. These pros bring insider knowledge, securing you the latest plans and better rates.

They also steer you through regulatory waters. (Did you know that in New York, small businesses with 1-100 employees have to offer health insurance?) A savvy broker keeps you in compliance and free from penalties.

Regular Reassessment

The health insurance scene is like shifting sand. Make a habit of a yearly check-up on your coverage. Last year’s winner could be this year’s dud.

These strategies will help you safeguard your team’s well-being and your business’s future. (It’s a win-win for everyone, really.)

Final Thoughts

So, small businesses – they’re swimming in a sea of health insurance choices, right? Each comes with its own shiny perks. From the old-school group plans to slick new ways like Health Savings Accounts… it’s all just evolving at warp speed. And here’s the thing: offering health insurance? It’s not just a checkbox. It’s a power move. The kind that reels in top talent, cranks up productivity, and yep, scores you some sweet tax benefits.

Picking that just-right health plan? It’s like a puzzle. You gotta dive deep into your team’s needs. It’s all about the balance – costs versus coverage. Plus, keeping things flexible is key. And don’t forget, give that plan a regular once-over. Because changes in your business mean what worked yesterday might not cut it tomorrow.

Over at Insurance 2ALL, we’ve turned guiding small businesses through the health coverage maze into an art form. Personalized support? Check. We’ll help you nail down affordable, top-tier solutions that sync up with your business dreams and what your employees actually want (no sneaky extra fees, promise). We break down the jargon, streamline it all, so you can zero in on scaling your biz while making sure your team stays healthy and happy.