Getting laid off? Yeah, that blows—especially when you’re scrambling to keep your health coverage. But fear not. At Insurance 2ALL, we totally get it: landing that free health coverage when the paychecks dry up is crucial.

Here’s the deal… we’re diving into three biggies: Medicaid, the Affordable Care Act Marketplace, and COBRA. (I know, acronyms… bear with me.) We’re talking eligibility, benefits, how to apply—the whole shebang—so you can make the call on what works best for your healthcare needs.

Medicaid: A Lifeline for Low-Income Individuals

Understanding Medicaid Eligibility

Alright, so Medicaid… it’s not just another government program. It’s a genuine lifeline for folks without a job. (Yes, a lifesaver.) This blend of federal and state efforts throws a health insurance buoy to millions-yes, millions-of Americans grappling with income constraints.

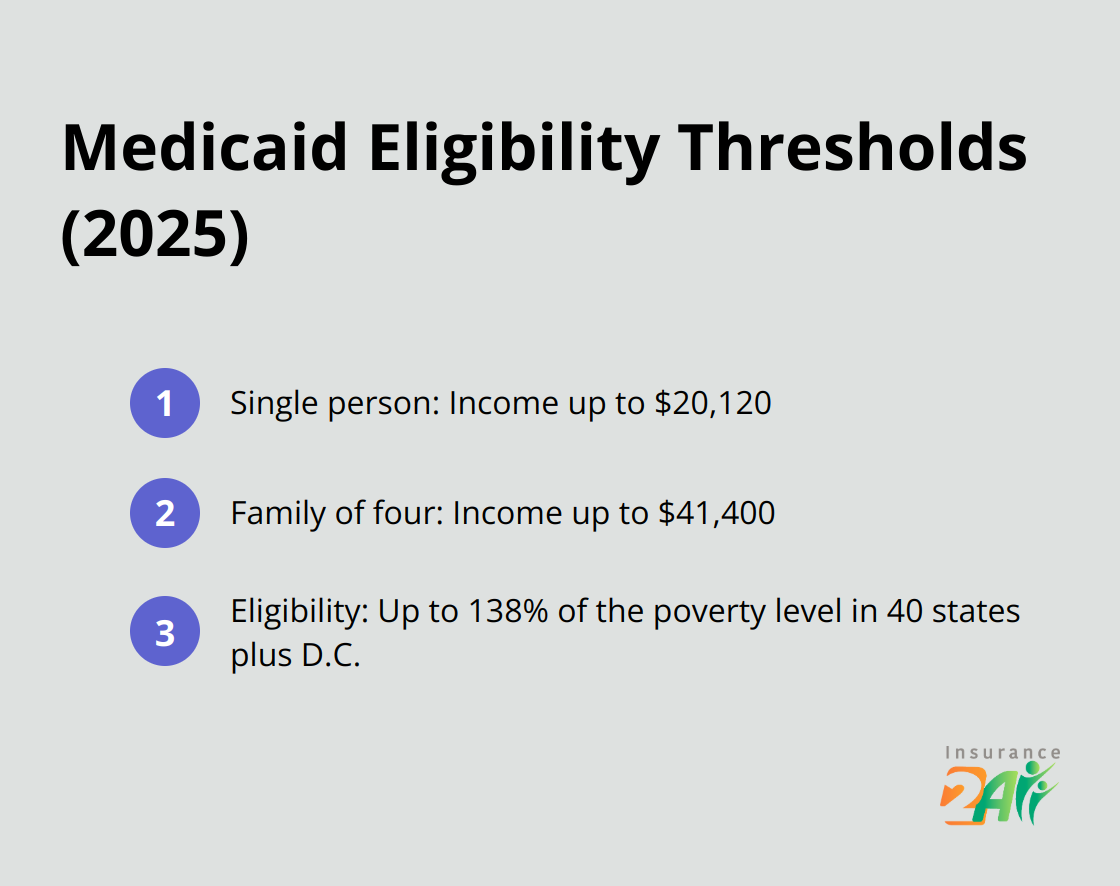

Now, the rules of the game? These could shift depending on your zip code, but generally, this safety net is tossed to low-income adults, kids, expectant moms, seniors, and those with disabilities. Flash forward to 2025-you’ve got 40 states plus D.C. saying, “Alright, anyone under 65 and earning up to 138% of the poverty level? We’ve got your back.”

To give you an idea, in an expansion state this year, if you’re flying solo with an income up to $20,120, Medicaid steps in. Have a gang of four? That threshold climbs to $41,400. But heads up… numbers don’t stay static-always double-check your state’s latest figures.

Here’s a quick overview of Medicaid eligibility thresholds:

Comprehensive Coverage Benefits

When you think Medicaid, think of a well-stocked coverage basket. We’re talking essentials like:

- Doctor visits

- Hospital stays

- Preventive tune-ups

- Prescriptions

- Mental wellness care

What you’re getting with Medicaid is the full buffet: dental, vision, hospital stays (both in-and-out), drugs, and preemptive care at no cost. The best part? You’re not breaking the bank-services are mostly free or involve symbolic copayments. A solid choice for those with wallets feeling a bit light due to job loss.

How to Apply for Medicaid

So, now the million-dollar question… how to get in? The process-it’s user-friendly, though minor tweaks exist across states. Here’s the cheat sheet:

- Punch in “HealthCare.gov,” feed in your state and household info. This either leads you to your state’s Medicaid setup or the federal marketplace.

- Collect your paperwork: think proof of salary, residency, and citizenship.

- Fill it out-online, phone call, or at your local Medicaid HQ.

- Sit tight for the verdict. Most states wrap this up in around 45 days. (Pregnant? Disabled? It might be speedier for you.)

Remember, the Medicaid gates never close. Job off? You can apply whenever suits you.

Medicaid, no doubt, casts a wide net. But here’s the thing-don’t stick to one path. The Affordable Care Act (ACA) Marketplace? It’s another health coverage road, particularly if Medicaid’s not in the cards. Sneak peek: we’ll deep dive into how the ACA can catch you while you’re job-hunting in the next segment.

ACA Marketplace: Your Health Safety Net After Job Loss

Special Enrollment Period: A 60-Day Opportunity

So, you lost your job-big oof. But guess what? Losing that gig doesn’t mean you’re stuck without health coverage. Enter the Affordable Care Act (ACA) Marketplace with its 60-day Special Enrollment Period. It’s like a limited-time offer you need to jump on-fast. Lost your health coverage in the last 60 days? Perfect. You’ve got two months to get yourself a new health plan. But remember, tick-tock… this opportunity doesn’t last forever.

Subsidies and Savings: Affordable Coverage Options

Ah, subsidies-sounds boring but, oh, how they save you money. The ACA’s got your back with income-based subsidies that’ll put some cash back in your pocket. In 2023, a staggering 7.8 million folks on the ACA Marketplace scored Cost-Sharing Reductions (CSRs) along with premium tax credits.

Let’s break down the key benefits of ACA Marketplace subsidies:

What does this mean for you? Major savings on those pesky monthly premiums. Some people even manage to snag plans with premiums so low it’s almost unfair.

Plus, those cost-sharing reductions? They do wonders on your out-of-pocket costs for things like deductibles and copayments. More savings-yes, please.

Enrollment Steps: Five Simple Moves to Get Covered

- Hit up HealthCare.gov-or your state’s marketplace.

- Set up your account, fill out the application. (Pro tip: Have deets on your income, household size, previous coverage ready to roll.)

- Look through your plan options and compare the juicy details: premiums, deductibles, coverage. You know the drill.

- Pick your winner and get enrolled.

- Pay that first premium to activate your new coverage.

Little tip from me to you: Use the Marketplace’s comparison tool-it’s like having a cheat sheet to weigh costs and benefits, finding what fits just right for your needs and budget.

Your coverage kicks off on the first day of the month after that enrollment and payment. So, if you made it in on June 15 and paid up, congrats-you’re good to go by July 1.

Navigating Plan Options: Making an Informed Choice

The plan levels on the ACA Marketplace-Bronze, Silver, Gold, Platinum-it’s like finding the right dip for your chip. Each has its own cost structure and coverage vibe. Bronze means low premiums but high out-of-pocket, Platinum flips that script.

Balance your monthly budget with what you might need in healthcare. Think meds, planned procedures, ongoing conditions-all those fun adult things.

The ACA Marketplace? A rock-solid option for anyone newly unemployed and looking for health coverage. With its Special Enrollment Period, cool subsidies, and straightforward process, it’s pretty appealing. But don’t get tunnel vision. Next up-COBRA-another way to keep your healthcare steady after a job loss.

COBRA: Extending Your Previous Employer’s Coverage

What Is COBRA Coverage?

Let’s talk about COBRA – a mouthful, I know – but it stands for the Consolidated Omnibus Budget Reconciliation Act. It gives a lifeline… of sorts. You and your family, if you lose those precious health benefits, can choose to keep your group health plan for a bit longer, but only under certain circumstances.

Eligibility for COBRA

Here’s the deal: COBRA isn’t a free-for-all. You get dibs if:

- You worked for a company with at least 20 bodies on the payroll

- Job loss came knocking (and no, gross misconduct doesn’t count)

- Your working hours got slashed

- Life threw some other “qualifying events” your way

This perk also gives your spouse and kids a leg-up. Think about it – in 2021, around 155 million non-elderly folks had health coverage via their jobs (a potential horde of COBRA candidates if the axe fell).

Here’s what you need to know about COBRA coverage at a glance:

The Cost Factor

Brace yourself… COBRA isn’t cheap. You’re picking up the whole tab – yes, the whole thing, including what your employer used to chip in – and, surprise, a 2% admin fee. Here’s how it shakes out:

- Employers usually foot 83% of the singles’ premium

- For the whole fam, they cover about 74%

Without that safety net, brace for a sticker shock. Back in 2021, average annual premiums went for a ride:

- $7,739 if you’re single

- A jaw-dropping $22,221 if you’ve got family coverage

Yep, you’d pay all that… plus the extra 2% fee.

Duration of COBRA Coverage

Think of COBRA as a temporary bridge. It’s not forever. Usually gives you up to 18 months. But hey, if you’re disabled or hit another qualifying event, that bridge could stretch to 29 or even 36 months.

The Enrollment Process

Your ex-employer (or their insurance buddy) has to give you the 411 on COBRA within 14 days of your “qualifying event.” You’ve then got a 60-day clock ticking to make your move. Choose COBRA and then:

- Fill out that election form

- Hand it over to your plan’s gatekeeper

(Pro tip: COBRA is like a boomerang – coverage is retroactive if you opt-in. Wait out the full 60 days and buckle up to pay premiums all the way back to when coverage said goodbye. Bonus – you’re covered during those nerve-wracking decision days if you suddenly need medical help.)

Weighing Your Options

On paper, COBRA might look like a no-brainer. But hold your horses – it’s not always the magic bullet. Many folks sniff out cheaper options elsewhere. We at Insurance 2ALL are pros at helping clients unearth coverage choices that don’t torch their budgets. (Our squad is on standby to help you untangle the web of health insurance options after a job shake-up.)

Final Thoughts

So, you just lost your job and are wondering about health insurance? Panic mode, right? But hang on – losing a job doesn’t equal losing health coverage, and that’s a fact. Options like Medicaid, the ACA Marketplace, and everyone’s favorite acronym, COBRA, are there to catch you. They offer everything from free coverage to subsidized plans… basically, something for everyone. Keeping that safety net during unemployment? It’s key to dodging those nasty surprise medical bills and ensuring you can get the care you need.

Let’s recap the main takeaways from our health insurance deep dive:

- Medicaid offers comprehensive coverage for those with low income, with eligibility based on your household size and state.

- The ACA Marketplace provides subsidized plans with a 60-day Special Enrollment Period after job loss, potentially saving you big bucks on premiums and out-of-pocket costs.

- COBRA lets you keep your previous employer’s coverage, but at a higher cost. It’s a solid temporary option if you want to maintain your current plan.

Need a guide on this journey? Look no further than Insurance 2ALL – they’re like your GPS for navigating health insurance options. Their team? Absolutely dedicated to finding you a plan that fits like a glove. No financial nightmares here, just the support you need.

Why wait? Jump on this today and lock down your free health coverage while you’re out of work. With the right info and some backup, you’ll find a way to stay covered through this rollercoaster ride (even if it’s a bit bumpy at first). After all, your health? Priceless, no matter your employment situation.