If you’re shopping for health insurance for the first time, you’re not alone. An estimated 28 million Americans remain uninsured in 2025, many because navigating the options feels overwhelming. The stakes are real: a single hospitalization without coverage can cost tens of thousands of dollars. But here’s the good news: understanding the fundamentals of health insurance is simpler than you think. This guide walks you through the essentials—plan types, costs, coverage terms, and how to find affordable options that actually fit your life.

Key Takeaways

- 28 million Americans lacked health insurance in 2025, but 93.3% of marketplace enrollees receive tax credits to reduce costs (2025, CDC & Pew).

- Understanding deductibles, copays, and coinsurance is the foundation of choosing the right plan—premiums alone don’t tell the full cost story.

- HMO, PPO, and EPO plans trade flexibility for affordability; pick based on whether your doctors are in-network and whether you value specialist freedom.

- What Health Insurance Covers: Medical services funded by your insurer after you meet your deductible, including preventive care, hospitalization, and prescription drugs.

- Plan Types (HMO/PPO/EPO): HMOs are cheapest but restrictive; PPOs are flexible but pricier; EPOs balance both with no out-of-network coverage except emergencies.

- The Cost Terms You’ll See: Premiums, deductibles, copays, and coinsurance all add up—knowing the difference helps you pick the right plan.

- Where to Find Affordable Plans: ACA marketplaces, employer coverage, Medicare for seniors, and private brokers like Insurance 2All can help match you to plans with available subsidies.

- Enrollment Periods Matter: Open enrollment happens annually; missing it means waiting a year unless you qualify for a special enrollment period due to life changes.

What Is Health Insurance and Why Do You Need It?

Health insurance is a contract between you and an insurance company that covers part or all of your medical costs. When you get sick or injured, your insurance picks up the bill—at least after you pay your share. Without it, a single hospital stay can cost $15,000 or more out of pocket. With insurance, you’re protected from catastrophic medical debt, and you also get access to regular preventive care that keeps you healthier in the first place.

“Health insurance sets an annual out-of-pocket maximum, meaning once you’ve spent a certain amount, the plan covers 100% of your care for the rest of the year. That ceiling protects you from financial ruin.”

How Health Insurance Protects Your Finances

Think of health insurance like a safety net. If you break your leg or develop an infection, your insurance covers the majority of treatment costs. You pay a monthly premium upfront, then additional costs when you use care (your deductible, copay, or coinsurance). But here’s the key: insurance sets an annual out-of-pocket maximum, meaning once you’ve spent a certain amount, the plan covers 100% of your care for the rest of the year. That ceiling protects you from financial ruin. In 2024, the ACA out-of-pocket maximum was $9,450 per individual, after which your plan pays all remaining covered medical expenses.

Types of Coverage Available

You have several paths to health insurance. ACA/Obamacare plans through the marketplace are available to anyone and often come with government subsidies if you qualify by income. Employer-sponsored plans are offered through your job and often cost less because your employer shares the premium. Medicare coverage kicks in at age 65 for seniors. And if you’re self-employed or between jobs, you can buy individual plans directly from insurers or through a broker like Insurance 2All who specializes in matching you to the right option with available subsidies and personalized guidance.

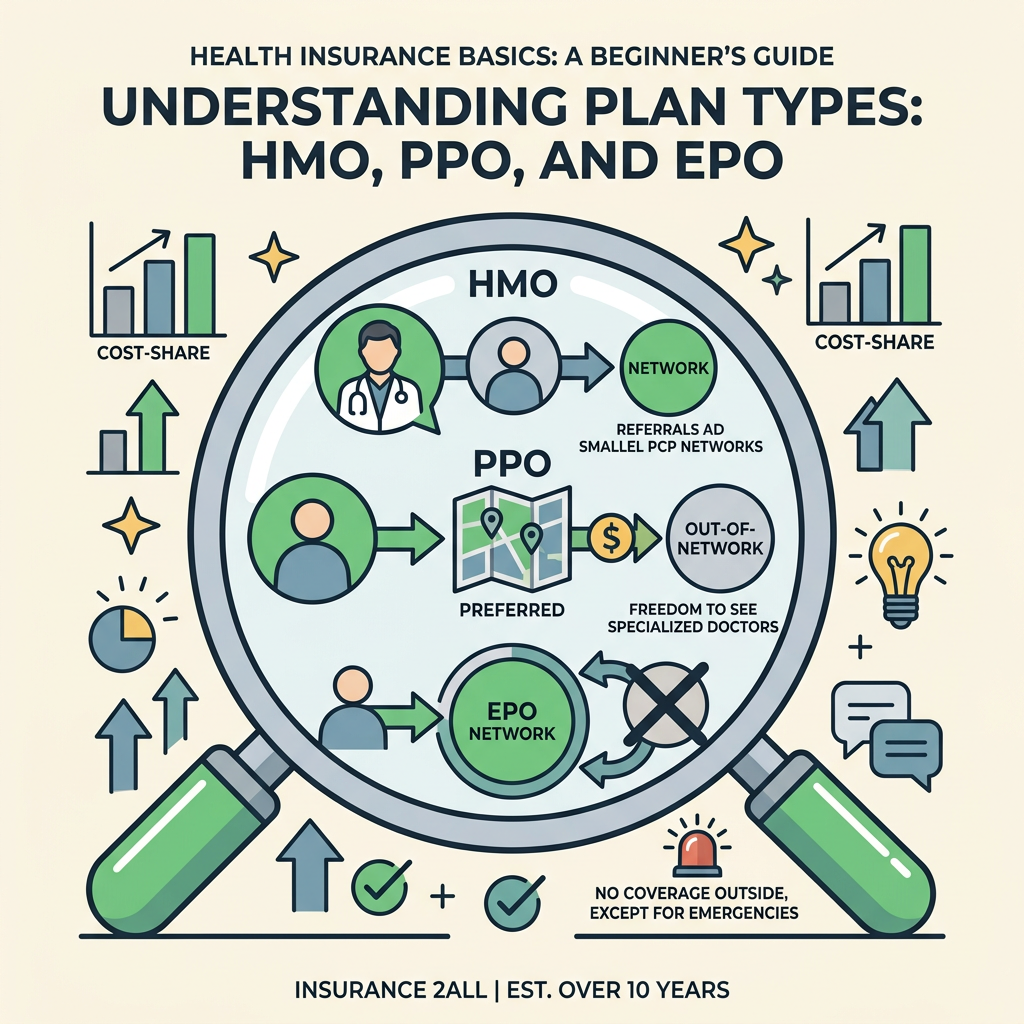

Understanding Plan Types: HMO, PPO, and EPO

The most confusing part of health insurance for beginners is the alphabet soup of plan types. HMO, PPO, and EPO all work differently—and the choice between them can save or cost you hundreds of dollars a year. The key difference is how much freedom you have to choose your doctors and whether you need referrals to see specialists. According to Aetna, understanding these differences is the fastest way to match your actual healthcare needs to the right plan. Here’s what you need to know to pick the right one.

How HMO Plans Work (and When to Choose One)

An HMO (Health Maintenance Organization) is the budget-friendly option. You pick a primary care doctor, and if you need a specialist, your primary doctor has to refer you. HMOs require you to use in-network doctors except in emergencies—step outside the network and you pay the full cost. Because of these restrictions, HMOs have the lowest premiums and often the lowest total costs if you stay in-network. They work best if your doctors are already in the plan’s network and you don’t mind the referral process. Aetna and Blue Cross both offer HMO plans, and they typically appeal to individuals and families comfortable with a single provider network and willing to keep routine care simple.

“HMOs are the budget-friendly choice for people whose doctors are already in-network and who value simplicity and cost savings over flexibility.”

How PPO Plans Work (and When to Choose One)

A PPO (Preferred Provider Organization) is the flexibility option. You don’t need a primary doctor or referrals. You can see any specialist whenever you want, and you can even go out-of-network—though you’ll pay more for it. PPOs have higher monthly premiums than HMOs, but they’re worth it if you travel frequently, have complex medical needs, or want the freedom to choose your own specialists without asking permission. Healthcare.gov notes that PPOs are the most flexible network-based option for people who value provider choice. UnitedHealthcare and other major carriers offer PPO plans that appeal to people who value provider choice above cost savings.

How EPO Plans Work (and Why They’re Growing)

An EPO (Exclusive Provider Organization) splits the difference. Like an HMO, you must use in-network providers except for emergencies—no out-of-network coverage otherwise. But like a PPO, you don’t need referrals to see specialists. Premiums are usually between HMO and PPO levels. EPOs work well if you want specialist freedom and a smaller network cost structure, but you’re comfortable staying in-network for routine care. They’re increasingly popular because they offer a practical middle ground for people who want access without premium sticker shock.

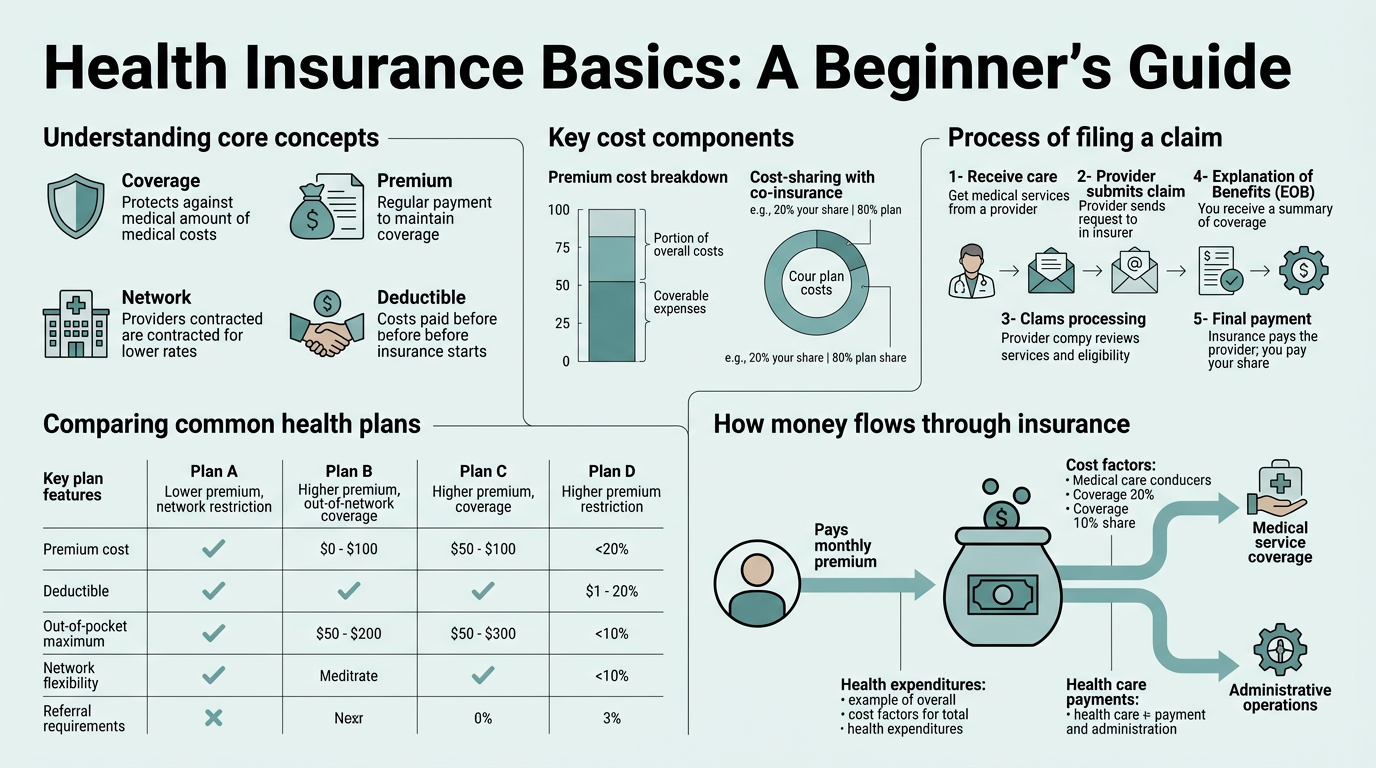

Breaking Down Health Insurance Costs

Most beginners focus on monthly premiums and ignore everything else—then get shocked when they owe thousands at the doctor’s office. The truth is, your total cost comes from four different places: premiums, deductibles, copays, and coinsurance. Understanding how they work together is the single most important skill for choosing the right plan.

“Low-premium plans often have higher deductibles, while higher-premium plans come with lower deductibles and out-of-pocket costs. The best choice depends on whether you use healthcare frequently or rarely.”

Premiums, Deductibles, and Your Annual Out-of-Pocket Maximum

Your premium is the monthly bill you pay whether you use health care or not. It’s the price of having coverage. Your deductible is the amount you must pay out of pocket before your insurance kicks in. If you have a $2,000 deductible and visit the doctor, you pay the full cost until you’ve hit $2,000. After that, your insurance starts covering services (though you still pay copays and coinsurance). The catch: plans with lower premiums often have higher deductibles. A plan that costs $150/month might have a $3,000 deductible, while a $300/month plan might only have a $1,000 deductible. Your annual out-of-pocket maximum is the most you’ll pay in a year. In 2024, the maximum was $9,450 for individuals. Once you hit that number, your plan pays 100% of covered expenses for the rest of the year.

Copays and Coinsurance: What You Pay at the Doctor

After you meet your deductible, you typically still pay something when you use care. A copay is a fixed amount—like $30 for a doctor visit or $15 for a prescription. Coinsurance is a percentage of the cost—like 20% of a specialist visit. Both count toward your annual out-of-pocket maximum. The strategy? Compare the total: low-premium plans often mean higher deductibles and copays, while higher premiums can mean lower out-of-pocket costs if you use a lot of care. That’s why many families with regular doctor visits or prescription medications choose a plan with a higher premium but lower deductible—the math works out cheaper overall.

| Plan Type | Typical Premium | Typical Deductible | Network Requirement | Referrals Needed? |

|---|---|---|---|---|

| HMO | $150–$300/month | $1,000–$3,000 | In-network only (except emergencies) | Yes, for specialists |

| PPO | $250–$450/month | $1,500–$5,000 | In-network preferred, out-of-network allowed | No |

| EPO | $200–$350/month | $1,000–$3,500 | In-network only (except emergencies) | No |

| Insurance 2All Broker Service | Covers all types | Matches to your budget | Personalizes network fit | Bilingual guidance included |

Essential Health Insurance Terms You’ll Encounter

Health insurance has its own language. Before you sign up for any plan, get familiar with these core terms—they’re the foundation of understanding what your coverage actually includes and what you’ll have to pay.

Coverage Basics: What’s In and What’s Out

Most health insurance plans cover preventive services (annual checkups, vaccines, cancer screenings) at no cost to you, emergency care, hospitalization, prescription drugs, mental health services, and maternity care. What they typically don’t cover: cosmetic procedures, experimental treatments not approved by the FDA, and care outside the United States (though travel insurance can help). Each plan has a formulary—a list of covered drugs. If your medication isn’t on it, you either pay more or ask your doctor to prescribe something on the list. Pre-existing conditions are protected by law, meaning insurers can’t deny you coverage or charge more because of past health issues.

Special Situations: Coordination of Benefits and Prior Authorization

Coordination of benefits applies if you have two insurance plans (like through your job and your spouse’s job). The insurers figure out how much each pays so you’re not overpaid. Prior authorization is when your insurance company requires your doctor to get permission before certain tests or treatments. It sounds annoying, but it’s designed to make sure you get necessary care, not unnecessary (and expensive) procedures. If your doctor wants to order an MRI or a specialist visit, your insurance might say “yes, we’ll cover that” or “no, try physical therapy first.” Understanding your coverage before you need it prevents surprises later.

How to Find and Choose an Affordable Health Insurance Plan

Finding the right plan for your situation doesn’t have to be a guessing game. There are several paths, each with different advantages—and knowing which path works for you saves time and money. The best plan is the one that covers your doctors and medications at a price you can actually afford.

Using the ACA Marketplace and Tax Credits

The ACA marketplace (healthcare.gov or your state’s website) is open every fall for annual enrollment. You can browse plans, compare costs, and see if you qualify for advance premium tax credits—subsidies that reduce your monthly premium. In 2025, 93.3% of marketplace enrollees received tax credits, making plans significantly more affordable. If you’re self-employed, unemployed, or don’t have employer coverage, the marketplace is your first stop. You choose your plan, enroll, and coverage begins January 1st (or the 1st of the month after enrollment if you apply later). If you’re between jobs, you may also qualify for COBRA (continuing your old employer plan) or marketplace coverage, and a broker can help you compare which is cheaper for your situation.

Employer Plans and Group Coverage

If you work full-time, your employer likely offers health insurance. The advantage: your employer covers part of the premium, which usually makes it cheaper than buying on your own. The catch: you’re limited to the plans your employer offers, and coverage typically starts on your hire date or the first of the month after your hire date (varies by employer). If your spouse works, you might compare their employer plan against yours before enrolling. If you’re self-employed or run a small business, group plans for small business owners are available and often come with tax advantages.

Working With an Insurance Broker

An insurance broker like Insurance 2All works with multiple insurers and knows the ins and outs of different plans in your state. Rather than you doing the comparison shopping alone, a broker saves you time by narrowing options to what actually fits your budget and medical needs. They also specialize in bilingual support, which is invaluable if English isn’t your first language. Importantly, brokers don’t charge you directly—they’re paid by insurers—so you get personalized guidance at no additional cost. For many families, especially those navigating subsidies or complex situations (like someone with a pre-existing condition), a broker is worth its weight in gold.

Qualifying Life Events and Special Enrollment Periods

Most people enroll in health insurance during the annual open enrollment period in the fall. But if your life changes—marriage, divorce, job loss, or a new baby—you get a special enrollment period. This allows you to sign up or change plans outside the regular window, usually within 30–60 days of the qualifying event.

Qualifying Events That Open the Door

You qualify for a special enrollment period if you lose your job and your employer’s coverage ends, get married or enter into a domestic partnership, have a baby or adopt a child, divorce or end a domestic partnership, move to a new state, or lose coverage from another source (like your parent’s plan if you’re turning 26). Each event has its own timeline—usually 30 to 60 days to enroll in a new plan. Missing the deadline means you’re stuck uninsured until the next open enrollment period unless you can appeal. That’s another place where a broker helps: they know the rules and deadlines, and they file your special enrollment application correctly so you don’t lose eligibility.

What Happens After Enrollment

Once you enroll, your coverage starts on a specific date (usually the first of the month). You’ll receive an insurance card in the mail and login credentials for the insurer’s website, where you can verify your coverage, check your deductible status, and access your provider network. When your new health coverage begins, use the first month to verify that your doctor is in-network and confirm any prescriptions are on your plan’s formulary. If something’s wrong or missing, contact your insurer or broker immediately—the first 30 days are the easiest time to make changes.

Tips for Choosing the Right Plan as a Beginner

You now understand the basics. Here’s how to turn that knowledge into a smart choice.

- Start with your doctors: Look up whether your current doctor is in-network for each plan you’re considering. A cheap plan is no deal if it doesn’t include your doctor.

- Check your prescriptions: Confirm that any medications you take are on the plan’s drug formulary. If they’re not covered or covered at a high tier, factor that into your cost estimate.

- Estimate your annual medical costs: If you visit the doctor frequently or have chronic conditions, add up premiums + expected copays and deductibles. Compare that total across plans, not just the premium.

- Consider your life stage: Young and rarely sick? A low-premium, high-deductible plan might save money. Family with kids or ongoing health needs? Pay more upfront for a lower deductible to keep total costs down.

- Don’t ignore subsidies: If you’re buying on the ACA marketplace, check whether you qualify for tax credits. Many people don’t apply because they assume they don’t qualify—but the income limits are higher than most think.

- Get help if you’re overwhelmed: Talking to a broker at Insurance 2All costs you nothing and can save thousands by matching you to the right plan and subsidies from day one.

Conclusion

Health insurance basics come down to a few core ideas: understand your premiums, deductibles, copays, and coinsurance; know the difference between HMO, PPO, and EPO plans; and match the plan to your doctors, medications, and budget. With 28 million Americans uninsured and over 93% of marketplace enrollees receiving tax credits, affordable coverage is available—you just have to know where to look and what questions to ask. The time you spend understanding these fundamentals now saves you money, stress, and surprise medical bills later. Ready to find your plan? Contact Insurance 2All today for personalized, bilingual guidance that matches you to affordable coverage.

FAQs

What is the difference between HMO and PPO health insurance?

The main difference is flexibility versus cost. HMOs require you to use in-network doctors and get referrals for specialists, but premiums are lower. PPOs let you see any doctor without referrals and cover out-of-network care (though you pay more for it), but premiums are higher. Choose an HMO if your doctors are in-network and you want the lowest cost. Choose a PPO if you value provider freedom or expect to need out-of-network specialists. EPOs offer a middle option: no referrals needed, but you stay in-network except emergencies, with premiums between HMO and PPO.

How much does health insurance cost per month?

Monthly premiums for individual coverage range from $150 to $450 depending on plan type and your age. HMOs average $150–$300, PPOs $250–$450, and EPOs $200–$350. But premiums don’t tell the whole story—you also pay deductibles, copays, and coinsurance when you use care. If you qualify for ACA subsidies (which over 93% of marketplace enrollees do), your premiums can drop significantly. The best way to estimate true costs is to add premiums, expected copays, and typical deductibles together, then compare plans on that total rather than premium alone.

What health insurance do I qualify for?

Most people qualify for at least one of three types: employer plans (if your job offers them), ACA marketplace plans (open to anyone and often covered by subsidies), or Medicare (if you’re 65 or older or disabled). The best path depends on your situation: employment status, age, income, and whether you have dependents. A broker like Insurance 2All can review your specific circumstances—whether you’re self-employed, between jobs, a recent graduate, or a family—and identify which programs and plans you’re eligible for, including subsidies and cost-sharing reductions. Contact them for a free consultation.